Table of Contents

Key Takeaways

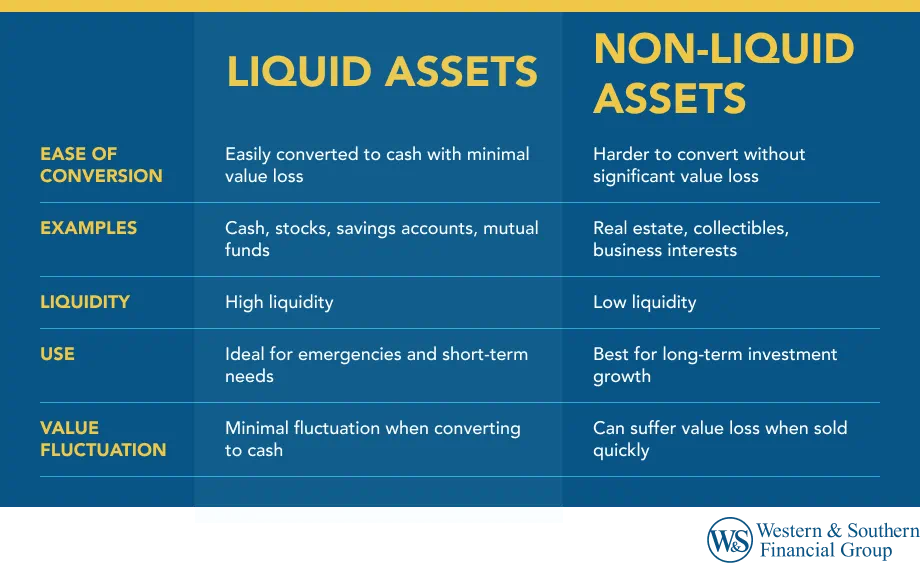

- Liquid assets are easy to turn into cash with little loss in value, making them ideal for covering unexpected expenses.

- Non-liquid assets are harder to convert into cash and often lose significant value if there are few buyers when you need to sell.

- Examples of liquid assets include cash in checking, savings, money market, and certificate of deposit accounts, as well as some life insurance policies.

- Non-liquid assets like real estate, business interests, jewelry, and cars may appreciate over time but can be difficult to sell quickly.

- Consulting a financial advisor can help you find the right balance of liquid and non-liquid assets to meet your financial goals and prepare for emergencies.

As you build wealth, it's important to understand where your money is and how you can use it. Since you most likely have short- and long-term goals, you may want to include a variety of tools within your financial strategy to accommodate those different types of goals.

Knowing the difference between liquid vs. non-liquid assets can thus help you identify how various savings and investment approaches could fit into your overall financial plan.

What Are Liquid Assets?

Liquid assets can be converted to cash with little impact to the overall value. It's important to have liquid assets for situations when you need money quickly. For example, cash in your checking account is liquid. If you face unexpected expenses for medical care or car repairs, funds in your checking account are available to pay expenses immediately.

A few examples of liquid assets are:

- Cash in checking, savings, and money market accounts

- A mutual fund or ETF (exchange-traded fund)

- Certificates of deposit (A CD may be liquid, depending on its terms and charges.)

- Life insurance cash value (Cash value can be liquid, but if your policy has a surrender charge early on, it may not be considered a liquid asset for a certain number of years.)

- Annuities (If your policy has a surrender charge early on, an annuity may not be considered a liquid asset for a certain number of years.)

It's important to keep in mind that qualified accounts may not be considered liquid if you are under the age of 59 1/2 and early tax penalties apply.

What Are Non-Liquid Assets?

Non-liquid assets can be difficult to convert into cash or cash value, and can come with a significant loss in value. For instance, real estate is never liquid. You might have significant equity in your home, but using that equity to pay for the costs associated with a sudden health emergency may be challenging. One option is to sell your home, but that may be an outsized effort that could take several months, not to mention the transaction fees and the need to move. You could also apply for a second mortgage, which involves its own set of complications and fees (for example, you'd need a willing lender and would add a lien on your home).

Although non-liquid assets are hard to convert, you can sometimes accelerate the process. For example, you could offer to sell non-liquid assets at "fire-sale" pricing (well below their market values). This may lead to a loss but if the asset has gone up in value, the price you sell it for could be more than what you invested.

A handful of examples of non-liquid assets are:

- Investment real estate (Real estate may take time to sell and requires significant effort to convert into cash.)

- Business interests (These may require finding a buyer with the skill, experience and capital needed to keep the business running.)

Other non-liquid assets could also include tangible items such as personal real estate, jewelry and cars. Non-liquid assets can be difficult to convert into cash or cash value, resulting in a significant loss in value.

Benefits & Stipulations of Liquidity

It might make sense for your financial plan to include both liquid and non-liquid assets, but you need to understand how each type of asset may affect your finances.

- Liquid assets can provide flexibility. If you need to spend money, you can get funds quickly from liquid sources. Money placed in Federal Deposit Insurance Corporation (FDIC)-insured bank accounts is also insured (up to the $250,000 limit per account) in case the bank fails, which is unlikely.1

- Non-liquid assets may be harder to cash out, and they could come with a loss in value. For example, a tangible non-liquid asset may depreciate in value. However, it's also possible that you could sell the asset for more than what you originally invested.

Many people keep both liquid and non-liquid assets in order to help diversify their wealth. Having liquid assets on hand can help if you have an immediate need for cash. If you keep too much in non-liquid assets, you may be forced to make sacrifices or take on debt whenever you need to raise cash.

The Bottom Line

As with many other things in personal finance, the balance of liquid vs. non-liquid assets that works best for you will depend on your own financial goals, and how you plan to fund them. Consider consulting with a qualified financial representative to help ensure you have adequate liquidity should an emergency arise.

Sources

- Deposit Insurance FAQs. https://www.fdic.gov/resources/deposit-insurance/faq/index.html.