Table of Contents

Key Takeaways

- Annuities have two phases, accumulation phase and payout phase, and they provide a steady income stream in retirement.

- Fixed annuities guarantee a certain interest rate for a specific period, while variable annuities offer investment options with higher growth potential and higher risk.

- A Rollover IRA allows you to transfer funds from a previous employer's 401(k) into a traditional IRA, providing tax advantages and continued tax-deferred growth.

- Compound interest is interest earned on both the principal amount and accumulated interest over time, leading to significant growth potential.

- Beneficiaries receive assets after your death, and trusts manage and distribute those assets.

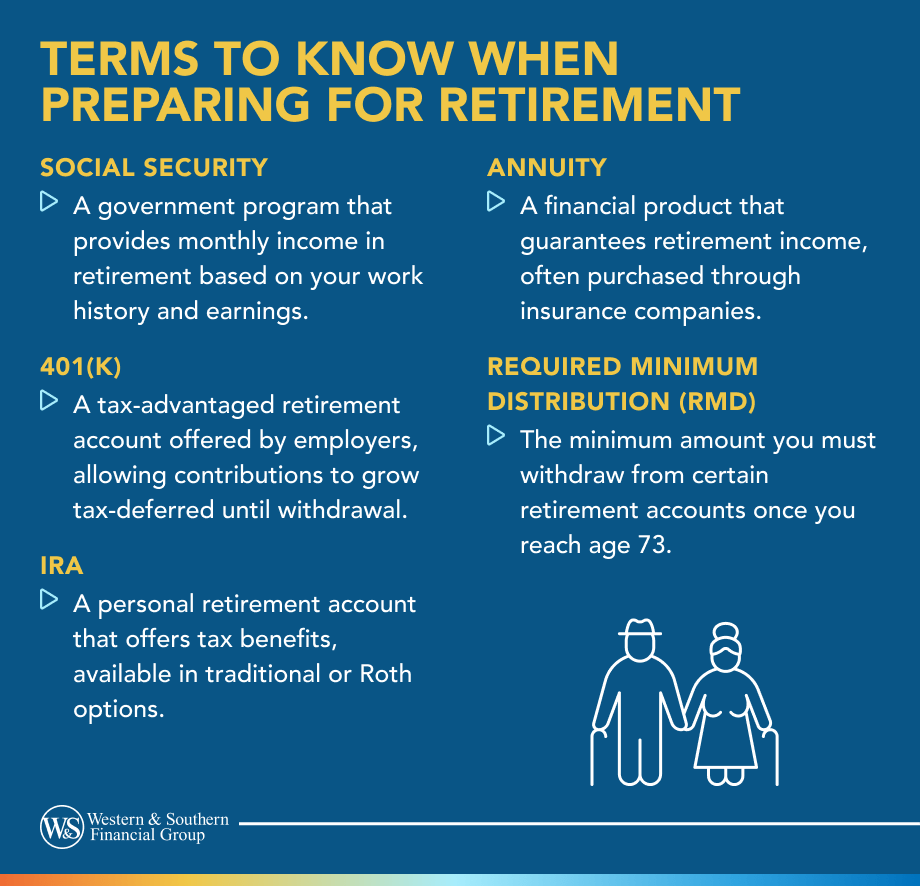

Retirement terms can be confusing but understanding some of the common vocabulary can be important as you start planning for your golden years. Here are some of the terms, and their meanings, to know.

Annuities

An annuity could help you with your living expenses in retirement. Annuities have two phases:

- Accumulation phase, when you make payments and you have the potential for interest earnings to build

- Payout phase, when you receive payments from the annuity

There are several different types of annuities. The kind you might choose depends on whether you're in the planning stages of retirement, and are saving up for it, or are already retired. Here are a couple of the common different types:

Fixed Annuity

With a fixed annuity, you're guaranteed a certain interest rate for a given period of time. When that period ends, the insurer will declare a new interest rate and guaranteed amount of time. Interest earned is tax-deferred, which means you won't owe taxes until you start taking distributions.

Variable Annuity

Variable annuities allow you to allocate your funds among a variety of investment options, which are called subaccounts, with risk tolerances that range from conservative to aggressive. The return on your investment depends on the performance of the underlying investments of the subaccounts, so there is a higher rate of risk in return for higher growth potential. You may not owe taxes on your earnings until you start taking distributions.

Rollover IRA

When you switch jobs, you have several options for handling the existing funds in your 401(k) account. One option is a rollover individual retirement account (IRA), which involves the transfer of funds from other sources such as a 401(k) into a new or existing traditional IRA. You may not have to pay taxes on the rollover as long as it's completed within 60 days of the initial distribution.

Other advantages? That money will continue to grow tax-deferred. Since the rollover from your former employer's 401(k) account to the rollover IRA isn't categorized as a contribution, there's no cap on the rollover amount.

Compound Interest

Compound interest is a common term, and it refers to interest earned on interest. The further in advance you save, the greater potential your contributions have for growth.

Consider these two scenarios: First, say you deposit $5,000 into an account with compound interest rate of 6 percent semiannually. Then you let the money sit for 25 years. In addition to earning interest on the money you invest, you also earn interest on that interest at the end of every compounding period. After 25 years, your initial deposit will have grown to almost $22,000.

Second, say you deposit $5,000 into an account with simple interest rate of 6 percent, which is just interest earned on the original amount. After 25 years, you will have earned $7,500 in interest for a total of $12,500.

Beneficiary

A beneficiary is a person, such as a spouse or child, or entity, such as a charity or business, that's designated to receive a death benefit, money, asset, etc. when you die. Choosing the beneficiaries of your assets is a serious decision. You could name multiple beneficiaries and distribute your payout among them. Or you could decide to name a primary beneficiary and a contingent beneficiary. The primary beneficiary receives your payout when you die. However, should they die before you do, the payout will be passed to the named contingent beneficiary.

Trust

When you're creating an estate plan, you have the choice of establishing what's called a trust. It's a legal arrangement you make with a third party. This third party, called a trustee, has the right to hold assets for a beneficiary or beneficiaries. There are many different types of trusts, and each is designed with a specific goal in mind.

The Bottom Line

By understanding these basic retirement terms, you may be better informed to make the right decisions when planning for your retirement years. If you have additional questions about planning for retirement, consider speaking with a financial representative, and if you have additional questions about trusts, consider speaking with an estate attorney.