Asset Allocation Chart of the Month

Earnings Growth Remains Strong and is Broadening

- Second quarter earnings season has gotten off to a very strong start. More than one quarter of S&P 500 companies have reported results, with 86% exceeding earnings expectations. This is well above the historical average in the high 70% range.

- The magnitude of earnings surprises has been even more impressive. Reported earnings have come in 39% above expectations, although Alphabet accounted for a disproportionate share of that upside. Even excluding Alphabet, earnings have exceeded estimates by nearly 13%, which is almost double the historical average of about 7%.

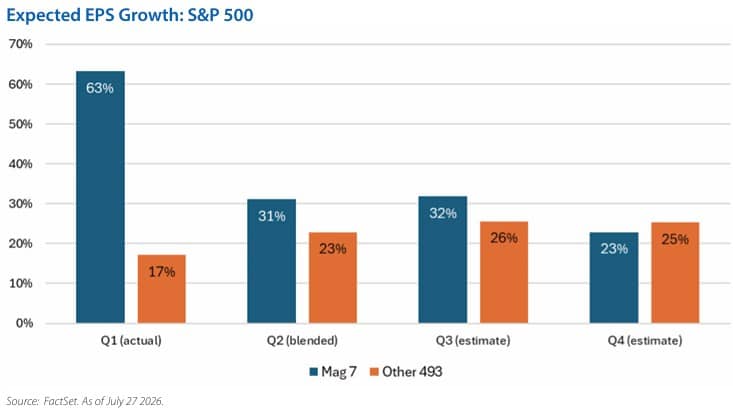

- While AI-related companies continue to lead earnings growth, the story is becoming increasingly broad-based. Excluding the Magnificent 7, the remaining 493 companies are on pace to deliver their strongest quarterly earnings growth since late 2021.

- Perhaps more importantly, analysts expect this broadening to continue. By the fourth quarter, earnings growth for the S&P 493 is projected to modestly exceed that of the Mag 7, suggesting improving profit momentum across a wider range of sectors and industries.

- The key takeaway: Corporate earnings remain exceptionally strong, but the drivers of that growth are becoming more diversified. While AI leaders continue to generate outstanding profits, earnings momentum is spreading across a broader set of companies and sectors, creating a healthier foundation for the equity market. For investors, that is an encouraging development. A broader earnings recovery creates more opportunities beyond the AI leaders and reinforces the value of active management in identifying companies positioned to benefit from expanding profit growth.

The Touchstone Asset Allocation Committee

The Touchstone Asset Allocation Committee (TAAC) consisting of Crit Thomas, CFA, CAIA – Global Market Strategist, Erik M. Aarts, CIMA – Vice President and Senior Fixed Income Strategist, and Tim Paulin, CFA – Senior Vice President, Investment Research and Product Management, develops in-depth asset allocation guidance using established and evolving methodologies, inputs and analysis and communicates its methods, findings and guidance to stakeholders. TAAC uses different approaches in its development of Strategic Allocation and Tactical Allocation that are designed to add value for financial professionals and their clients. TAAC meets regularly to assess market conditions and conducts deep dive analyses on specific asset classes which are delivered via the Asset Allocation Summary document. Please contact your Touchstone representative or call 800.638.8194 for more information.

A Word About Risk

Fixed-income securities can experience reduced liquidity during certain market events, lose their value as interest rates rise and are subject to credit risk which is the risk of deterioration in the financial condition of an issuer and/ or general economic conditions that can cause the issuer to not make timely payments of principal and interest also causing the securities to decline in value and an investor can lose principal. When interest rates rise, the price of debt securities generally falls. Longer term securities are generally more volatile. Investment grade debt securities may be downgraded by a Nationally Recognized Statistical Rating Organization to below investment grade status. Non-investment grade debt securities are considered speculative with respect to the issuers' ability to make timely payments of interest and principal, may lack liquidity and has had more frequent and larger price changes than other debt securities. Equities are subject to market volatility and loss. Growth stocks may be more volatile than investing in other stocks and may underperform when value investing is in favor. Value stocks may not appreciate in value as anticipated or may experience a decline in value. Stocks of large-cap companies may be unable to respond quickly to new competitive challenges. Stocks of small- and mid-cap companies may be subject to more erratic market movements than stocks of larger, more established companies. Investments in foreign, and emerging market securities carry the associated risks of economic and political instability, market liquidity, currency volatility and accounting standards that differ from those of U.S. markets and may offer less protection to investors. The risks associated with investing in foreign markets are magnified in emerging markets, due to their smaller and less developed economies.

The information provided reflects the research and opinion of Touchstone Investments as of the date indicated, and is subject to change without prior notice. Past performance is not indicative of future results. There is no assurance any of the trends mentioned will continue or forecasts will occur. Investing in certain sectors may involve additional risks and may not be appropriate for all investors. The indexes mentioned are unmanaged statistical composites of stock or bond market performance. Investing in an index is not possible. For Index Definitions see: TouchstoneInvestments.com/insights/investment-terms-and-index-definitions

Please consider the investment objectives, risks, charges and expenses of the fund carefully before investing. The prospectus and the summary prospectus contain this and other information about the Fund. To obtain a prospectus or a summary prospectus, contact your financial professional or download and/or request one on the resources section or call Touchstone at 800-638-8194. Please read the prospectus and/or summary prospectus carefully before investing.

Investment return and principal value of an investment in a Fund will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. All investing involves risk.

Touchstone Funds are distributed by Touchstone Securities, LLC*

*A registered broker-dealer and member FINRA/SIPC.

Touchstone is a member of Western & Southern Financial Group

Not FDIC Insured | No Bank Guarantee | May Lose Value