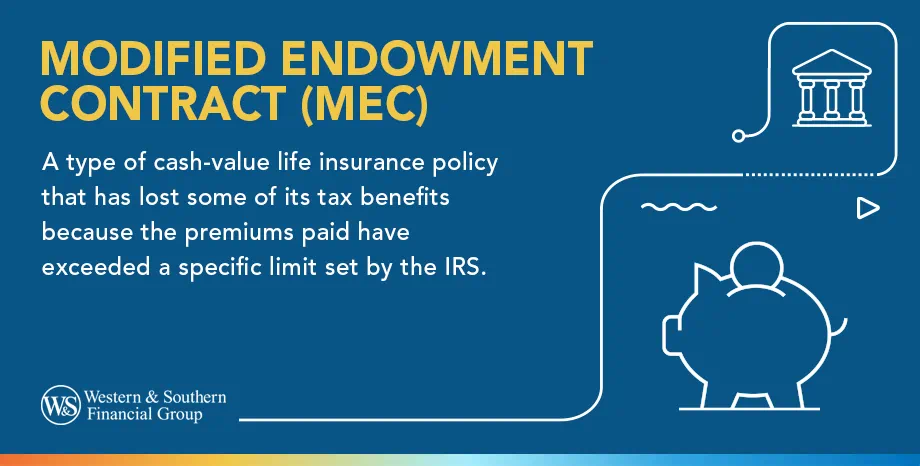

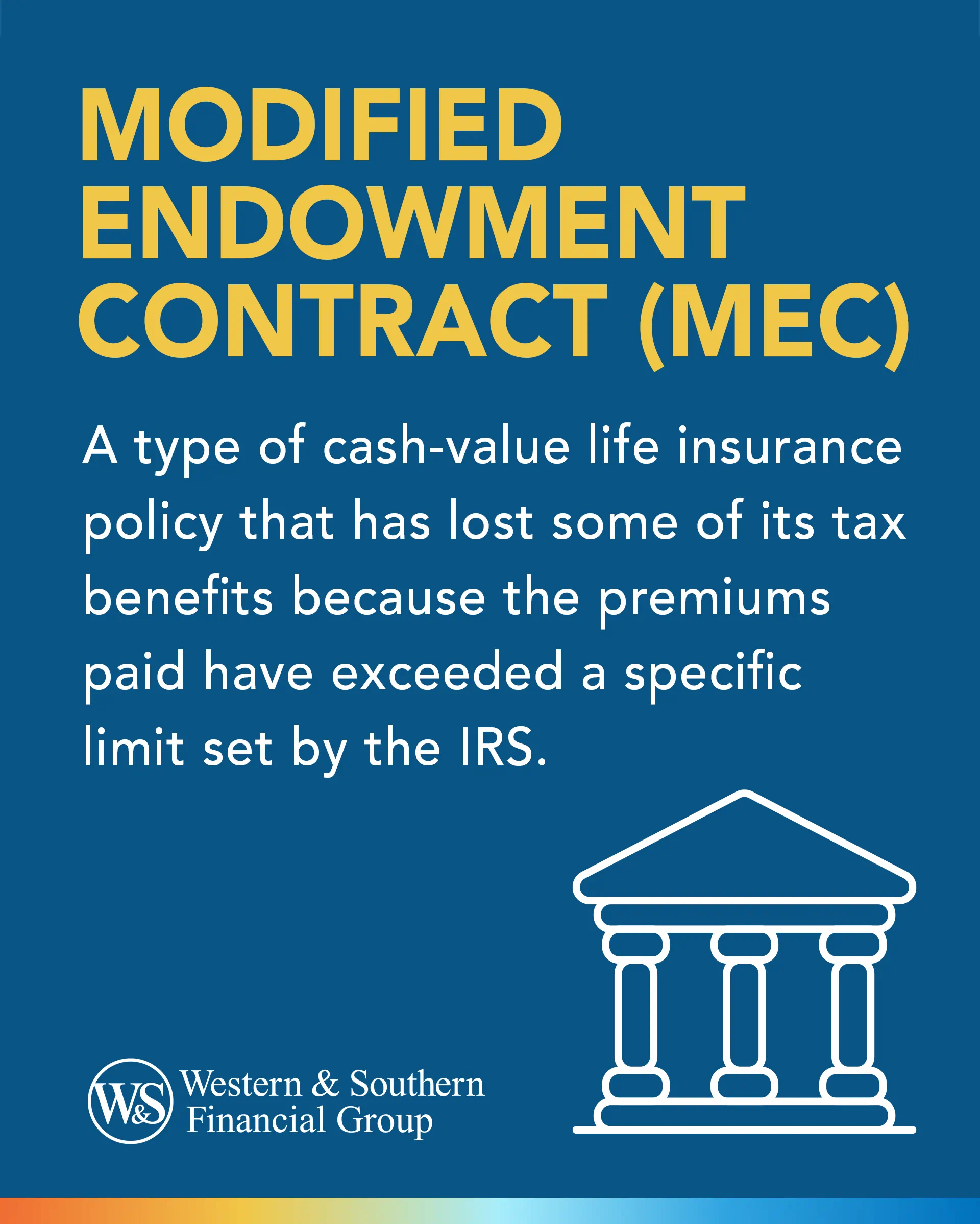

What Is a Modified Endowment Contract?

A Modified Endowment Contract (MEC) can be any life insurance policy that accumulates cash value and where the premiums paid exceed certain IRS limits under the 7-pay test. MECs lose the typical tax benefits of life insurance policies, leading to potential tax implications on withdrawals and loans. Understanding MECs is crucial for maximizing the benefits of your life insurance.

Background

MECs originated in the late 1980s after interest rates on cash-value life insurance policies hit a jaw-dropping 20 percent. In addition to their impressive interest rates, these policies avoided the taxes more traditional investments faced because of how the IRS taxed permanent cash-value life insurance policies.

Tax-deferred cash value grows without tax, and the first-in, first-out (FIFO) method is used to withdraw the funds. That means you can access your money tax-free up to the cash value of the contributions you've paid through your premiums. You can also take a tax-free loan from the cash value (although such a loan may create an income-tax liability, be subject to interest, reduce the cash value and death benefit, and cause the policy to lapse).

Before the advent of MECs, investing a large sum of money in a small permanent life insurance policy was possible, effectively creating a potentially high-growth tax shelter. As a result, Congress passed the Technical and Miscellaneous Revenue Act (TAMRA) of 1988, which instituted MECs. TAMRA was implemented to discourage investors from using life insurance to avoid federal income taxes.

What is the Seven-Pay Test?

As part of the TAMRA implementation, the legislation limits how much you can pay into a life insurance policy over a set period. Exceeding the limits set by the IRS will result in the policy becoming an MEC.

These limits are called the "7-pay test." A policy will fail the 7-pay test and trigger a MEC if the policyholder pays premiums over the amount needed for the policy to be paid up in seven years.

Once a life insurance policy becomes a MEC, it cannot be reclassified as a traditional life insurance policy. If there's an accidental overage, the Internal Revenue Service (IRS) gives your life insurance provider 60 days to return the overfunded amount to you before a MEC triggers.

The 7-pay test is generally used only in the first seven years after purchasing a policy unless there's a material change to the policy, such as a reduction in the death benefit or the addition of a life insurance rider, in which case a new 7-pay test must be run.

Example

Here's a basic example of how a policy might become a Modified Endowment Contract (MEC):

Scenario: Suppose John purchases a whole life insurance policy with a death benefit of $500,000. He wants to ensure that the policy also serves as a vehicle for saving and potentially accessing cash in the future. To accelerate the growth of the policy's cash value, John decides to pay significantly higher premiums in the early years.

Action: In the first year, John pays an annual premium of $20,000. He continued to pay $20,000 annually for the next six years.

- Totaling $140,000 in cumulative premiums over the first seven years.

Seven-Pay Test: According to the IRS's 7-pay test, John could have paid the maximum amount into the policy over seven years without turning it into a MEC. Let's say, for simplicity, this amount is $100,000 for his policy.

- John's total premiums paid ($140,000) exceed this limit ($100,000).

Resulting Status: John's policy is classified as a Modified Endowment Contract (MEC) because his premiums in the first seven years exceeded the amount specified by the 7-pay test.

Avoid unintended MEC classification and optimize your life insurance strategy. Get a Life Insurance Quote

How Do I Know if My Policy Is a MEC?

- Check the Seven-Pay Test: The IRS compares your total premiums paid in the first seven years to a calculated premium limit. If your premiums exceed this limit, your policy becomes a MEC.

- Look for MEC Designation: Your insurance company should notify you if your policy is classified as a MEC. Life insurance companies typically perform monthly MEC tests to alert policyholders of potential overfunding before triggering the MEC.

- Consult a Financial Advisor: Your financial advisor or life insurance agent can assess your policy and help you understand its MEC status.

What Types of Life Insurance Policies Could Be a MEC?

The most common types of life insurance coverage options that could potentially become MECs include:

- Whole Life Insurance is the most typical type for which a MEC status is likely due to its inherent cash accumulation benefits and premium payment structure.

- Universal Life Insurance offers flexibility with its premiums and benefits, but it can quickly become a MEC if significant premiums are paid early to accelerate cash value growth.

- Variable life insurance, like universal life, invests a portion of the premium in accounts that can vary with the market. However, making high premium payments that quickly raise the cash value can lead to MEC classification.

- Indexed Universal Life Insurance is a type of universal life insurance in which the cash value growth is tied to a stock index. If not monitored carefully, aggressive policy funding can trigger the MEC status.

In all these cases, the classification as a MEC depends on the premiums paid relative to the amount that would pay up the policy within seven years, according to the IRS's 7-pay test.

Life insurance policyholders should consult their financial advisor or life insurance agent to carefully manage premium payments to avoid unintended MEC classification, especially when aiming to maximize the tax-advantaged growth of the policy's cash value.

Tip

For policyholders who specifically want a MEC, single-premium life insurance is considered one from the outset because it's funded with a single, significant premium.

Tax Implications

The tax implications of a MEC are significantly different from those of a non-MEC life insurance policy, primarily impacting the taxation of withdrawals and loans.

- Taxation of Withdrawals and Loans: Unlike non-MEC policies where withdrawals up to the total amount of premiums paid are tax-free and withdrawn on a first-in, first-out (FIFO) basis, withdrawals from a MEC (including loans taken against the policy) are taxed on a last-in-first-out (LIFO) basis. This means any gains in the policy are taxed as ordinary income before any principal is withdrawn.

- Early Withdrawal Penalties: If the policyholder takes a withdrawal or loan from a MEC before the age of 59½, they will not only owe income tax on the gains but also a 10% federal penalty on the amount of the gains withdrawn, similar to early withdrawals from an IRA or 401(k).

- Tax-Free Death Benefit: A MEC's death benefit remains generally tax-free to beneficiaries, consistent with other life insurance products. However, the less favorable treatment of other disbursements during the policy's life (such as loans and withdrawals) often makes MECs less attractive for those seeking the policy for investment and cash liquidity purposes.

Because of these implications, policyholders and potential life insurance buyers should carefully plan premium payments and understand whether a regular life insurance policy might become a MEC. Financial planning around a MEC should consider these tax consequences to optimize the policy's tax benefits and avoid unexpected tax liabilities.

Pros: Benefits of a MEC

Despite the stricter tax rules associated with MECs, there are certain advantages to holding a MEC, particularly for individuals with specific financial goals and situations. Here are some of the benefits:

- Tax-Deferred Growth: Like other permanent life insurance policies, a MEC allows the cash value component to grow tax-deferred. This means that interest, dividends, and capital gains within the policy accumulate without being subject to taxes until they are withdrawn.

- High Contribution Limits: MECs do not have the annual contribution limits typical of other tax-advantaged accounts like IRAs or 401(k)s. This can make MECs an attractive option for individuals who want to invest large sums in a tax-advantaged vehicle, especially those who have already maxed out other retirement accounts.

- Estate Planning Benefits: A MEC's life insurance death benefit is generally tax-free to the life insurance beneficiaries, which can be a significant advantage for estate planning purposes. It provides a means to pass wealth to heirs without income tax liabilities and, with proper planning can also help reduce estate taxes.

- Asset Protection: In many jurisdictions, the cash value and death benefits of life insurance, including MECs, are protected from creditors. This can make MECs useful for asset protection strategies, particularly for business owners and professionals in high-liability careers.

- No Mandatory Withdrawals: Unlike certain retirement accounts, MECs do not require minimum distributions at any age. This can provide more flexibility in financial planning, allowing policyholders to decide when or if they want to access their funds for retirement income based on their financial needs.

Cons: Drawbacks of a MEC

While Modified Endowment Contracts (MECs) offer certain benefits, there are also notable drawbacks to consider before choosing this type of policy. Here are some of the main disadvantages:

- Taxation on Withdrawals: One of the biggest drawbacks is the tax treatment of withdrawals and loans. Money taken from a MEC is taxed on a last-in-first-out (LIFO) basis, meaning that gains are taxed as ordinary income before any contributions are touched. This can lead to significant tax liabilities if large amounts of accrued gains are withdrawn.

- Early Withdrawal Penalties: If funds are withdrawn before the policyholder reaches the age of 59½, not only are the gains taxed as ordinary income, but a 10% federal penalty tax is also applied to those gains. This makes it less favorable for those needing early access to their funds.

- Loss of Favorable Tax Treatment for Premiums: Unlike premiums paid on non-MEC traditional life insurance policies, which can sometimes be accessed tax-free up to the amount paid in, MECs do not offer this benefit. This makes MECs less effective as a tool for tax-advantaged cash accumulation compared to other life insurance policies.

- Complexity and Monitoring: The rules surrounding MECs require careful monitoring of premium payments to avoid inadvertently triggering MEC status through excessive contributions. This complexity can make managing a life insurance policy more cumbersome and may require professional assistance.

- Inflexibility: Once a life insurance policy is classified as a MEC, it retains this status permanently. Even if premiums are reduced or stopped, the policy cannot revert to non-MEC status, limiting flexibility in how the policy can be managed or adjusted in response to changing financial circumstances.

These drawbacks mean that while MECs can be a powerful tool in specific situations, they are unsuitable for everyone. Potential buyers should consider their financial situation, future liquidity needs, and overall investment strategy before opting for a policy that may become a MEC.

The Bottom Line

Understanding the implications of a Modified Endowment Contract (MEC) is essential for any life insurance policyholder aiming to maximize their policy's benefits without unforeseen tax consequences. Staying informed about how MEC rules might affect your life insurance ensures your financial planning remains robust and proactive. Don't navigate this complex landscape alone; reach out to a trusted advisor today to review your policy and strategize effectively for your future needs.

Ensure your life insurance serves your financial goals without unexpected tax burdens. Get a Life Insurance Quote