Table of Contents

Key Takeaways

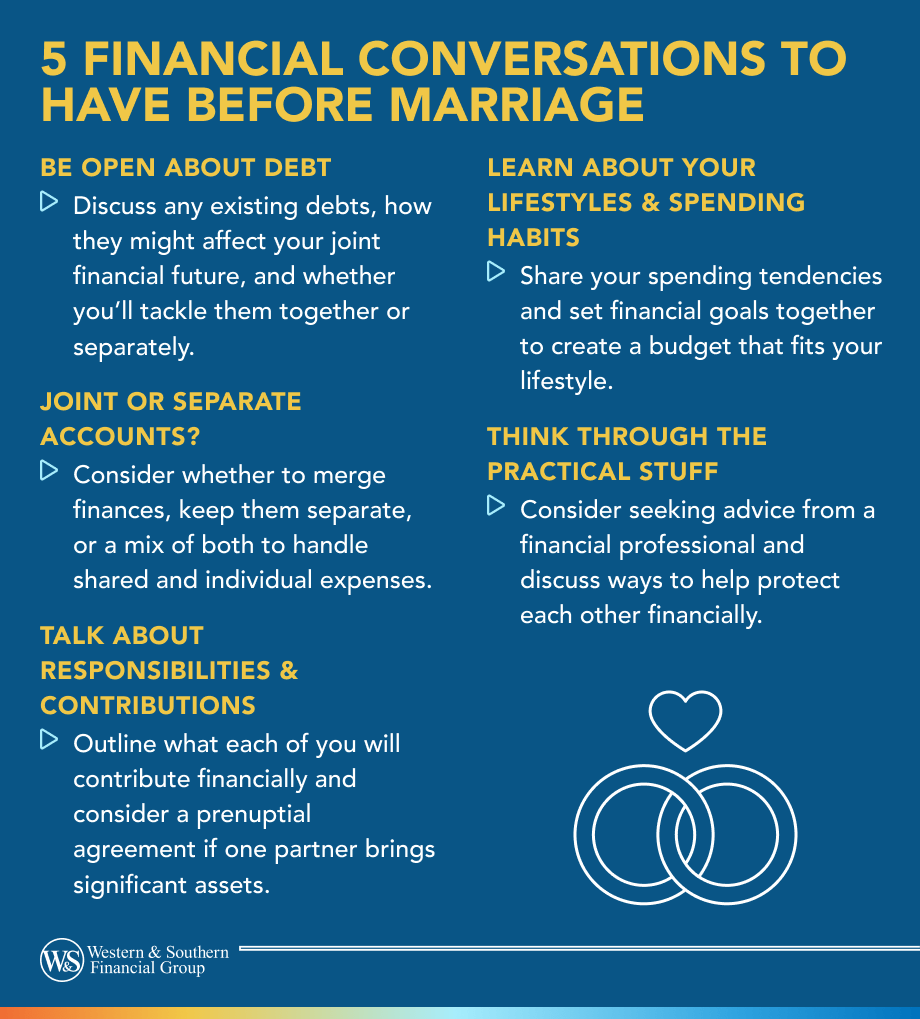

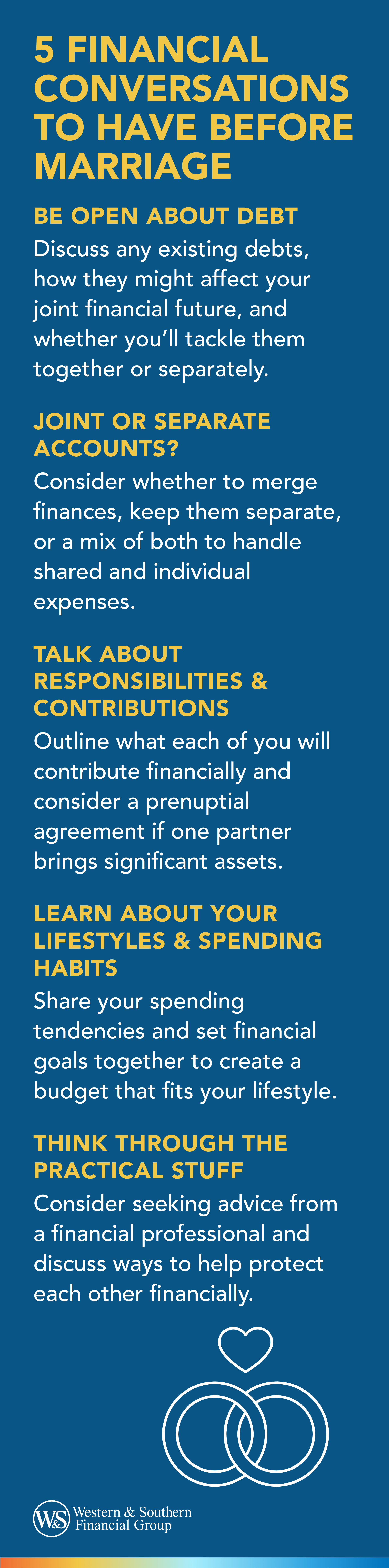

- Be transparent about any existing debt and make a plan for how you'll handle it jointly in the marriage.

- Decide whether you'll merge finances or keep separate accounts. You can also do a hybrid approach with joint and individual accounts.

- Discuss financial responsibilities and contributions openly. Consider a prenup if one partner has substantially more assets.

- Learn about each other's spending habits and lifestyle preferences to create a shared budget plan.

- Seek guidance from a financial professional to help create a financial plan and consider products like life insurance to protect each other.

Considering saying "I do"? Congratulations on taking this big step! You likely dream of happily ever after, but also consider practical talks like marriage finances. Maybe marriage and money don't sound all that romantic, but consider this: Finances are a leading cause of stress in relationships, and one of the main reasons couples say they fight.1

Addressing potential points of contention over money before you tie the knot — and being fully aware of what each of you brings to the relationship financially — may help you work better together as a married couple. Here are five money conversations to have before marriage so you can start your lives together on the same financial page.

1. Be Open About Debt

Your partner's debt could impact your credit score or ability to get a loan if you ever decide to apply for financing jointly (like when you go to buy a home). If either one of you carries a balance of any kind, make sure the other partner knows. Consider how you'll tackle that debt in your marriage: Will each person be responsible for paying off the debt they created outside the marriage on their own? Or will you work together to repay those balances?

Be aware of what liabilities each of you may bring to the table, and talk through a plan for dealing it before you legally bind yourselves — and your debts — together.

2. Decide: Joint or Separate?

Will you merge accounts? There's no one right answer, and every couple needs to decide for themselves what makes sense for their financial situation. If you can't agree or aren't sure of the best path to take, consider doing a little bit of both.

You can run your household and pay joint bills, like rent or a mortgage, from a jointly held checking account your paychecks go into. But you can also set up separate checking accounts each person can use for discretionary spending. Consider setting a budget that covers both joint and individual expenses.

You could, for example, agree that you each get $250 per month to spend on whatever you want — and keep that in your separate checking accounts.

3. Talk About Responsibilities & Contributions

Whether you merge your finances or keep money separate, be transparent about what you'll each bring to the relationship when you create your household together. If one or both of you are bringing in a large amount of assets, consider a prenuptial agreement. No, it's not exactly romantic — but it's the financially responsible thing to do to make sure both partners are protected in case something doesn't work out as planned.

When you look to the future, you probably can't say with any certainty that you'll always make this much and your spouse will make that much. And it's unlikely both you and your future spouse will make precisely the same amount of money and contribute exactly the same amount of time, effort and energy to your household 24/7.

That's OK. This is your relationship, which means you can create what you want. Talk through what you both want your roles and responsibilities to be. For every Plan A, make sure there's a Plan B if circumstances change. Be clear and open about what you can contribute, and ask for help in places where you fall short.

4. Learn About Your Lifestyles & Spending Habits

You love your partner, but that doesn't mean you love their inability to pass up an impulse buy every time they go shopping. Talk about your money habits, preferences, desires and fears openly — and without judging the other person.

Together, you can create a spending plan and budget that works for your income and allows you to enjoy your money without overspending or living above your means. It might help to set your financial goals together as you do this too, so you have something to motivate you both to stick to the plan and avoid blowing money on short-term gains or for instant gratification.

5. Think Through the Practical Stuff

If any of these conversations become too difficult to have on your own, you might want to head to a financial professional. A professional can not only help you create a plan, they can also serve as an objective third party who can help mediate financial discussions and provide guidance and advice to you both (so you don't get stuck arguing over which one of you is "right").

In addition to getting a financial plan to help you stay on track, talk to your partner about whether or not you may need to protect each other from financial hardship once you get married. Life insurance could offer peace of mind and help protect your partner against the uncertainties of life.

The Bottom Line

Although they're not fun to think about, these are practical measures you'll likely be happy you put into place. They can help provide peace of mind and confidence that you and your partner are taking care of each other — no matter what comes your way in marriage and in life.

Sources

- Looking for a Man in Finance: Money and Relationships. https://www.psychologytoday.com/us/blog/get-some-help/202410/looking-for-a-man-in-finance-money-and-relationships.