Should I Retire at 50?

To retire at 50, careful financial planning and consideration of expenses, health insurance, and inflation are crucial. It requires a substantial nest egg, taking stock of what you have, and covering costs for 30 or more years without income.

Consider your emotional readiness for retirement and the importance of having hobbies, interests, and a social network. Retiring at 50 can be the next step if you're financially stable, but consider working longer for a more secure foundation if there are uncertainties.

What Are the Average Retirement Savings at 50?

Retirement planning can be daunting, mainly when you aim to retire early. Understanding the average retirement savings at 50 can help provide a helpful benchmark as you plan for the future.

Many financial experts suggest saving about six times one's annual salary by age 50.1 This general guideline can vary based on individual circumstances, lifestyle choices, and retirement goals. According to the 2022 Federal Reserve's Survey of Consumer Finances, the average retirement savings for households aged 45 to 54 is around $115,000.2 However, this number might not be sufficient for those planning to retire at 50.

Retiring at 50 requires careful planning and disciplined saving. Tailoring your savings plan to your unique needs is essential. Consulting with a financial advisor can help you create a robust strategy for a comfortable retirement.

Remember, the earlier you start planning, the better prepared you'll be to enjoy your golden years without financial worries.

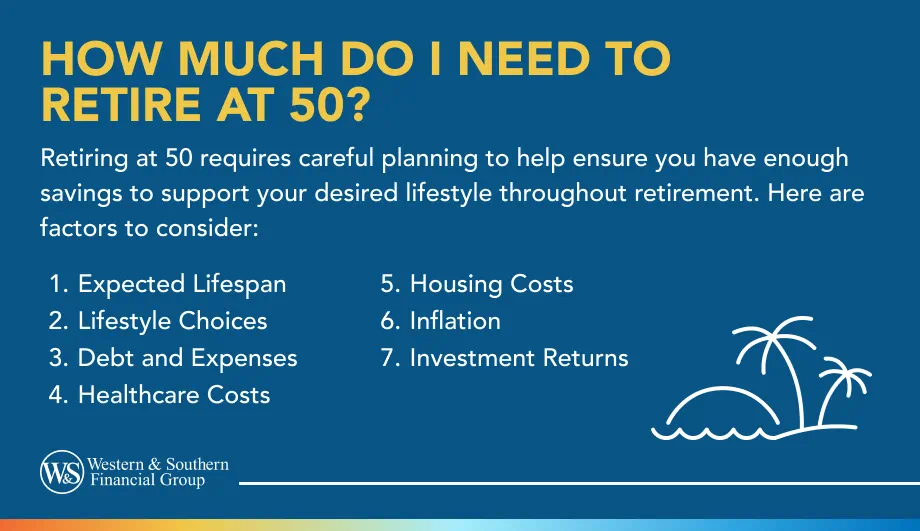

Factors That Affect How Much You'll Need To Retire

Retiring at 50 is essential to understand the factors that affect how much you'll need to retire comfortably. Here are the key considerations to keep in mind:

- Expected Lifespan: When preparing for retirement, it's essential to consider your expected lifespan. Planning for a longer life can help ensure you have enough money to cover your expenses.

- Lifestyle Choices: Your retirement savings depend on your lifestyle: you will need more if you plan to travel and dine out and less if you have a modest retirement lifestyle.

- Debt and Expenses: Existing debts and ongoing expenses impact your retirement funds. Paying off debts before retiring reduces monthly outflow and extends savings while knowing the expected costs is essential.

- Healthcare Costs: Healthcare costs in retirement are unpredictable and increase with age. Retiring at 50 requires covering 15 years of private insurance or out-of-pocket expenses before Medicare; set aside significant savings for this.

- Housing Costs: Housing costs are a significant part of your retirement budget, whether you own a mortgage or rent. Downsizing or moving to a lower-cost area can reduce expenses and stretch your savings.

- Inflation: Inflation reduces your money's purchasing power over time, meaning what costs $1,000 today may cost more in retirement. To maintain your lifestyle in retirement, invest in assets with good returns to help ensure your savings grow faster than inflation.

- Investment Returns: Investment returns significantly impact how much you need to retire at 50. Higher returns grow savings faster but with higher risks, so diversify your investments and work with a financial advisor for balanced growth and risk management.

Planning for retirement at 50 involves considering these factors and more. By carefully assessing all factors and planning accordingly, you can work towards a financially secure and fulfilling retirement.

Calculate Your Future Expenses

Estimating these expenses can help determine how much you need to save to retire comfortably. Here's a step-by-step guide to help you calculate your future expenses.

- Assess Your Current Expenses: Closely examine your monthly expenses, including housing, utilities, groceries, transportation, insurance, entertainment, and other regular costs. Knowing where your money goes now helps provide a baseline for your future budget.

- Estimate Healthcare Costs: Healthcare is a significant expense for retirees, including insurance, out-of-pocket, and long-term care. Before qualifying for Medicare at 65, you may need to purchase costly private health insurance.

- Factor in Inflation: Prices rise over time, so it's crucial to account for inflation in your calculations. Assuming an average inflation rate of 2-3% annually helps adjust estimates to accurately reflect future costs.

- Consider Lifestyle Changes: Consider how your lifestyle might change in retirement, such as increased travel, new hobbies, or more spending on leisure activities. Be realistic about these changes, as they can significantly impact your budget.

- Plan for Unexpected Expenses: Life is unpredictable, and unexpected expenses like home repairs or medical emergencies can arise. Set aside some of your savings as a financial cushion for these unforeseen costs.

- Calculate Your Retirement Income: Once you understand your future expenses, calculate your expected retirement income from savings, investments, pensions, and Social Security benefits. Compare this income to your estimated expenses to identify any gaps you need to fill.

- Adjust Your Savings Plan: If your expected income falls short of covering your expenses, it’s time to adjust your savings plan. This might mean saving more each month, investing in higher-yield assets, or even considering part-time work during retirement.

Calculating your future expenses is critical in determining how much you need to retire at 50. By carefully assessing your current spending, considering future changes, and planning for the unexpected, you can build a realistic budget to help you achieve your retirement goals.

Find out how much you need to retire comfortably at 50. Calculate Your Savings

Add Up All Your Potential Income Sources

Knowing the type of retirement income sources can help ensure a comfortable and stress-free retirement. Consider these key sources:

- Social Security Benefits: While you can't access Social Security benefits until age 62, including this in your long-term planning is essential. Knowing your estimated benefits can help you plan for the years beyond 50.

- Retirement Accounts: Primary income sources will be your 401(k), IRA, and other retirement accounts. Know the rules about early withdrawals and potential penalties; some accounts allow penalty-free withdrawals at 55, so check your specific plans.

- Pension Income: If you have a pension, it can be a stable and reliable income source. Understand your pension plan's details, including when payments start and the monthly amount you'll receive.

- Savings and Cash Reserves: Your savings and cash reserves will be crucial, especially in the first few years of early retirement. Help ensure you have a robust emergency fund to cover unexpected expenses without dipping into your retirement accounts.

- Annuities: Annuities can help provide a steady income stream for life. Calculate your expected monthly income and understand each type of annuity offers different benefits.

- Part-time Work: Many retirees find part-time work a fulfilling way to stay active and supplement their income. Whether consulting in your field, starting a small business, or working in a new area, part-time work can help provide financial and personal benefits.

By carefully considering and adding up all these potential income sources, you can create a comprehensive retirement plan at 50. Planning and understanding each income source can help you achieve a comfortable and fulfilling early retirement.

Planning Retirement Withdrawals

Knowing how much you need to retire at 50 involves more than just saving a large sum of money. You need a clear strategy for accessing and using those funds over what could be several decades of retirement.

- Estimate your retirement expenses, including housing, food, transportation, and healthcare. Consider travel, hobbies, and activities costs, noting that some expenses may decrease while others, like healthcare, may rise.

- Calculate your retirement savings by including all retirement accounts, such as 401(k)s, IRAs, and other investments. If you're retiring at 50, remember you won't access Social Security until 62, so your savings must cover a more extended period.

- Determining a sustainable withdrawal rate is crucial for retirement planning. While the 4% rule suggests withdrawing 4% of your savings annually, retiring early may require a more conservative approach to help ensure your savings last.

- When planning your withdrawals, consider the implications of taxes. Traditional retirement accounts like 401(k)s and IRAs are taxed as ordinary income, while Roth IRAs offer tax-free withdrawals; tax-efficient planning can help stretch your savings further.

- Plan for healthcare costs, especially if retiring before Medicare eligibility at 65. Help ensure coverage through private insurance or other means, and consider using Health Savings Accounts (HSAs), which offer tax-free withdrawals for qualified medical expenses.

- Create an emergency fund to handle unexpected expenses in retirement. This separate fund can prevent you from prematurely dipping into your retirement savings.

- Revisit and adjust your retirement plan regularly as your financial situation and spending needs change. Tracking your spending and adjusting your withdrawal strategy helps ensure your savings last throughout your retirement.

Retiring at 50 is ambitious but achievable with careful planning and a solid withdrawal strategy. Understand your expenses, calculate your savings, and make tax withdrawals; consider consulting a financial advisor to tailor your plan.

Tips for Retiring Comfortably at 50

Start Early and Save Aggressively

The earlier you start saving, the better. Aim to save at least 20% of your income, but if you can manage more, that's even better. Compounding interest works best over time, so starting in your 20s or 30s can make a significant difference by the time you hit 50.

Maximize Your Retirement Accounts

Take full advantage of retirement accounts like 401(k)s, IRAs, and Roth IRAs. Contribute the maximum allowed annually, and remember to take advantage of employer matches if available. These accounts offer tax advantages that can help your savings grow faster.

Diversify Your Investments

A diversified portfolio can help protect your savings from market volatility. It should include a mix of stocks, bonds, and other assets. Consider working with a financial advisor to create an investment strategy that aligns with your retirement goals and risk tolerance.

Reduce Debt and Manage Expenses

Paying off high-interest debt before retiring is crucial. This includes credit cards, personal loans, and even your mortgage. Lowering your monthly expenses can make your retirement savings last longer.

Calculate Your Retirement Needs

Understanding how much you need to retire at 50 involves estimating your annual expenses and determining how long your savings need to last. Consider factors like healthcare costs, inflation, and lifestyle changes. A common rule of thumb is to aim for 70-80% of your pre-retirement income.

Create a Detailed Retirement Plan

A comprehensive retirement plan includes your expected income sources, such as Social Security, pensions, and withdrawals from retirement accounts. Consider working with a financial planner to help ensure your plan covers all aspects of retirement.

Consider Health Insurance Options

Healthcare can be a significant expense, especially if you retire before you're eligible for Medicare at 65. Look into private insurance options or consider part-time work that offers health benefits.

Plan for Inflation

Inflation can erode your purchasing power over time. Help ensure your retirement plan includes a strategy to combat inflation, such as investing in assets that typically outpace inflation.

Be Prepared for the Unexpected

Life is unpredictable, and unexpected expenses can arise. An emergency fund can help provide a financial cushion without derailing your retirement plans.

Keep Revisiting Your Plan

Retirement planning is not a one-time task. To stay on track, regularly review and adjust your plan as needed. Changes in the market, your health, or your personal goals may require adjustments to your strategy.

Conclusion

With the proper planning and financial strategy, retiring at 50 is within reach. By understanding your expenses, potential income sources, and savings goals, you can create a roadmap to early retirement. Ready to take the next step? Work with one of our financial representatives to start planning your future today!

Begin today to learn how much you need to retire at 50. Start Your Free Plan

Sources

- Here’s how much money you should have saved at every age. https://www.cnbc.com/select/savings-by-age/.

- Survey of Consumer Finances (SCF). https://www.federalreserve.gov/econres/scfindex.htm.