Unlike the buzz of cryptocurrency investments or the instant gratification of new car, life insurance's true value lies in helping your loved ones from financial hardship. When acquired at a young age, it often costs less than monthly streaming subscriptions.

Why Young Adults Need Life Insurance

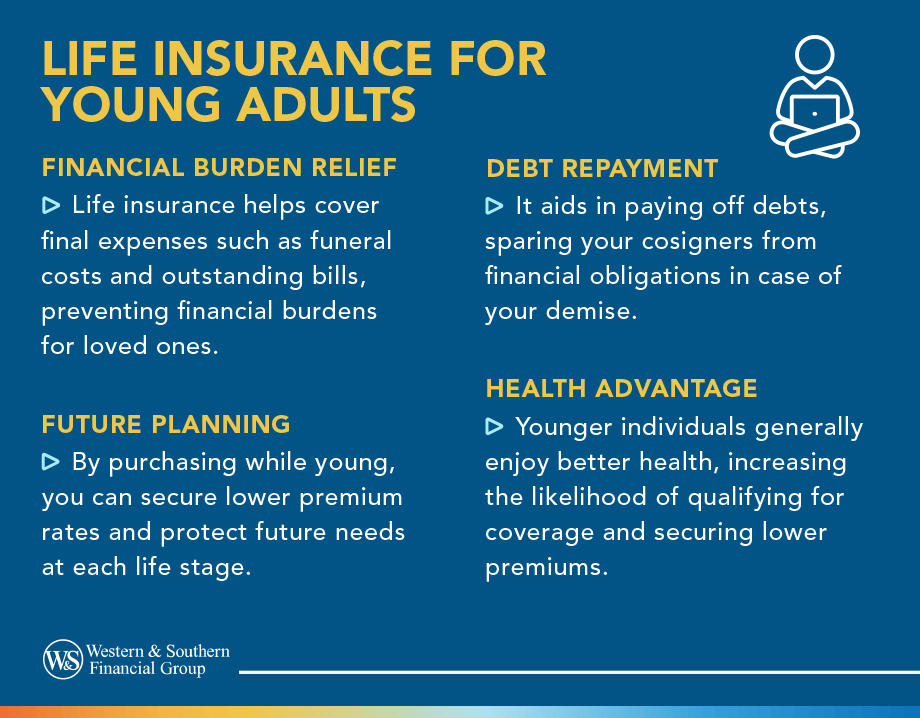

Most people think life insurance is just for settled down with a mortgage, kids, and retirement plans. However, your twenties and thirties are important for considering insurance due to these common factors:

The Health Advantage

Right now, you're probably in great shape; no worries about high blood pressure, cholesterol, diabetes, heart issues. Insurance companies know this and offer prices that match your healthy vibe.

For example: A healthy 25-year-old can get a 20-year, $500k life insurance policy for20-30/month. In ten years, the same policy may cost 50-100% more at age 35, especially with new health issues.

The Rate Lock-In

Depending on the type of life insurance policy, you could keep the same rate for the whole length of the term.

For example: Buy a 30-year policy at 25, and you pay 25-year-old rates until you're 55. Your monthly cost never increases, even as you age, even if you develop health issues.

The Future You're Building Toward

Student loans. Check. Maybe a car payment. Check. Thinking about buying a house someday? Check. Want kids eventually? Probably check.

Sure, you're single with no kids right now, but those future bills you're planning for make life insurance to think about. Plus, the longer you wait, the pricier those premiums get.

Understanding Your Life Insurance Options

Term Life Insurance: The Straightforward Option

Think of term life insurance as renting coverage. You pay a monthly premium for a set duration, usually 10, 20, or 30 years. If you die during the term, beneficiaries get the death benefit. If you outlive the term, the policy expires.

For most young adults, this can be a perfect fit because it's budget-friendly, easy to understand, and significant financial protection during the years when your earning potential is on the rise.

What Happens at the End of Term?

This is where people get confused. When your 20-year term ends at age 45, you don't just lose everything. You have options:

- Allow the policy to lapse if coverage is no longer necessary.

- Switch to a permanent policy, typically at a higher cost but without a new medical exam.

- Buy a new term policy, requiring updated underwriting based on your current age and health.

Permanent Life Insurance: The Long Game

Permanent policies, such as whole life insurance and universal life insurance, offer lifelong coverage. They never expire as long as you pay the premiums, but they do cost more than term for the same payout.

Who Should Consider Permanent Coverage?

Permanent policies make sense in specific situations:

- High net worth individuals facing estate tax implications

- Business owners needing insurance for buy-sell agreements

- People with lifelong dependents (such as disabled family members)

- Those maxing out other retirement income vehicles and seeking additional tax-advantaged accumulation potential

The Hybrid Middle Ground

Return of premium (ROP) term policies split the difference. You'll pay more compared to a term insurance, but if you outlive the policy, you'll get all your premium money back. However, ROP policies cost more than regular term insurance.

For some young adults, the 'refund guarantee' can be a reassuring feature, though it comes with higher premiums.

How Much Life Insurance Do You Actually Need?

The Single Young Adult

Even if you don't have children or responsibilities at this moment, you might still have:

- Student loans with a co-signer, often with a parent. Federal student loans are forgiven at death, but private loans may require co-signers to repay.

- Shared debts with a partner, roommate, or family member

- Pay for funeral expenses of loved ones

A life insurance policy could help covers these bases without breaking your budget. It can be enough to cover final expenses and help offer financial protection to anyone linked to you.

The Coupled Young Adult

In a relationship, whether married or not, the focus shifts toward income replacement to help ensure financial stability. If you contribute to household income, your death would create a financial gap.

Think about this when calculating your life insurance needs:

- Your annual salary × years until retirement

- Outstanding debts (mortgage, car loans, credit cards)

- Future financial needs (kids' college, major purchases)

It's a good idea to go for coverage that's about five to ten times what you make in a year.

The Parent

Having children transforms your financial priorities, as you'll be responsible for supporting them for the next 18 years or more. When calculating your coverage, consider:

- Childcare costs per year per child

- Education expenses averaging per child

- Housing stability

- Living expenses until children reach independence

What Affects Your Premium Rate?

Age: This is an important factor, as being younger generally means insurance companies consider you healthier.

Health Conditions: Some conditions (like well-controlled thyroid issues) have minimal impact, while others (like recent cancer diagnoses) may make coverage difficult to obtain.

Smoking Status: Insurance companies typically charge higher premiums for smokers and often require a tobacco-free period before offering non-smoker rates.

Family Medical History: Some policies consider a family's health history; early deaths from heart disease or cancer can increase rates.

Occupation and Hobbies: Dangerous jobs (logging, construction, law enforcement) or high-risk hobbies (skydiving, rock climbing, racing) may trigger additional premium costs.

Driving Record: DUIs and multiple moving violations can increase rates or complicate underwriting.

The Medical Exam: What to Expect

Most insurance policies require a medical exam. An examiner comes to your home or office at your convenience. They typically check:

- Height and weight

- Blood pressure

- Pulse rate

- Basic medical history

- Blood sample (cholesterol, glucose, liver function)

- Urine sample (drug screening, kidney function, sometimes nicotine)

Consult a financial expert to understand the process and learn how your costs are determined.

Special Considerations for Young Adults

Student Loans and Life Insurance

If you pass away, your federal student loans are wiped out. Your estate doesn't have to worry about paying them off. Some private lenders may pursue repayment from your co-signers if you pass away, while others might forgive the loan, so it’s important to review your loan terms carefully.

If you have private student loans with co-signers, life insurance equal to your outstanding balance protects them from inheriting your debt. As you pay down the loans, you can reduce your coverage amount.

The Employer Life Insurance Gap

Many young adults have life insurance through work, such as group term life insurance. But, it may not be sufficient nor does it travel with you when you leave the job.

Think of employer life insurance as a supplement, not a solution. Get your own policy independent of your job. The coverage follows you throughout your career.

The "Insurability" Window

You may not always be eligible to buy life insurance - certain health conditions, such as cancer, heart disease, or multiple sclerosis, may make you ineligible for coverage.

Your ability to qualify for insurance coverage is not guaranteed, as health can change unexpectedly. The time to buy life insurance is when you can easily qualify, not when you need it.

Common Mistakes Young Adults Make

| Mistake | Explanation |

|---|---|

| Waiting for the "Right Time" | Your ability to qualify for insurance coverage is not guaranteed, as health can change unexpectedly. |

| Not Buying Enough Coverage | While it may seem like a lot, medical bills, funeral costs, and lost income can deplete it quickly. |

| Thinking Premiums Are Expensive | Life insurance isn’t always costly; choosing the right policy helps balance affordability and protection. |

| Ignoring Conversion Options | Some term policies allow conversion to permanent coverage, so check if yours does. |

| Not Designating Beneficiaries | Not assigning beneficiaries can cause delays, as courts must appoint someone to manage minor heirs’ funds. |

| Forgetting to Pay Premiums | Automatic payments can fail, so it’s a good idea to review and update them each year to help keep your policy active. |

| Not Reading the Fine Print | Policies may exclude suicide, war, or aviation risks, so know what’s covered. |

Tips for Young Adults Before Buying Life Insurance

- Start Early While Rates Are Low: The younger and healthier you are, the lower your premiums will likely be. Buying early helps you lock in affordable coverage for decades.

- Match Coverage to Your Financial Situation: Opt for larger coverage if others depend on your income, or coverage for debts and final expenses if you have no dependents.

- Understand the Difference Between Policy Types: Term life is ideal for its low cost and simplicity; permanent life offers lifelong coverage and potential cash value.

- Take Benefit of Employer Coverage, but Don’t Rely on It: Employer-provided life insurance can be helpful, but having your own policy offers lasting coverage no matter where you work.

- Review Beneficiaries Regularly: As life changes - marriage, kids, or new financial goals - update your beneficiaries to reflect your current situation.

- Reassess Your Coverage Every Few Years: As your income, debt, and family situation change, revisit your policy to confirm it still meets your needs.

- Don’t Overlook the Tax Advantages: Life insurance often offers tax advantages, including generally income tax-free death benefits for beneficiaries, tax-deferred growth on cash value in permanent policies, and typically tax-free policy loans, though any unpaid loans may reduce the final payout. Tax-free assumes the policy is not a Modified Endowment Contract (MEC), the withdrawals do not exceed cost basis, and the policy does not lapse. Consult your tax advisor for specifics.

The Bottom Line

When you’re young and healthy, life insurance may not seem important, but waiting to get coverage can lead to higher costs or limited options later. A policy isn’t about you; it’s about protecting the people who depend on you - your partner, parents, children, or even a business partner - from financial hardship. For the cost of a few coffees a week, you can help support long-term financial stability.

It's never too soon to help protect your future with life insurance. Request a Free Life Insurance Quote

Sources

- Life Insurance Consumer Guide - National Association of Insurance Commissioners. https://content.naic.org/consumer/life-insurance.htm.

- Teenagers and young adults - Consumer Financial Protection Bureau. https://www.consumerfinance.gov/consumer-tools/money-as-you-grow/teen-young-adult/.

- Life Insurance Ratings and Financial Strength - AM Best Rating Services. https://web.ambest.com/.

- Tax Treatment of Life Insurance - Internal Revenue Service Publication 525. https://www.irs.gov/publications/p525.

- Student Loan Discharge in Case of Death - Federal Student Aid. https://studentaid.gov/manage-loans/forgiveness-cancellation/death.

- Estate Planning Basics - American Bar Association. https://www.americanbar.org/groups/real_property_trust_estate/resources/estate_planning/.