What is IUL Insurance?

Indexed Universal Life insurance (IUL) is a type of permanent life insurance policy that provides lifelong coverage and a cash value component, which grows based on the performance of a selected stock market index. IULs offer flexibility in premium payments, death benefits, and tax-deferred cash value growth. IUL policies combine life insurance protection with the potential for higher returns compared to traditional universal life policies while mitigating direct market risks.

What is Whole Life Insurance?

Whole Life Insurance is a type of permanent life insurance policy that provides lifelong coverage and includes a cash value component that grows at a guaranteed rate. Premiums are fixed, and the policy pays out a death benefit to your life insurance beneficiaries regardless of when the policyholder passes away. The life insurance cash value can also be borrowed against or withdrawn, offering a financial resource during the policyholder's lifetime. Doing so will reduce the death benefit and should only be done in emergency situations.

Key Differences Between IUL & Whole Life

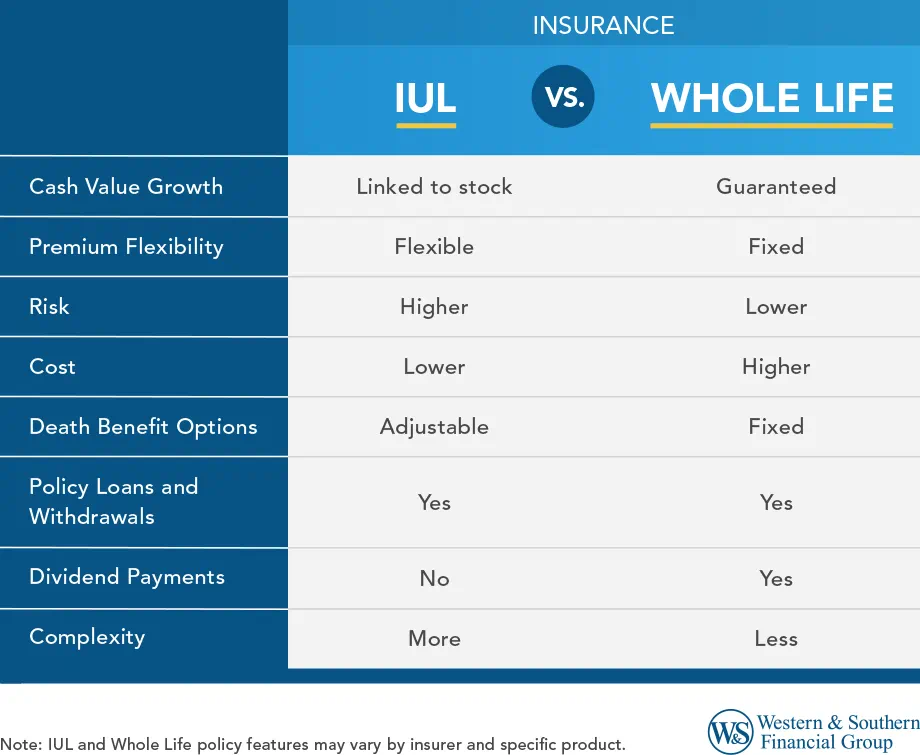

The key differences between an Indexed Universal Life insurance policy and a Whole Life insurance policy include:

- Cash Value Growth: IUL's cash value growth is linked to the performance of a stock market index, offering the potential for higher returns but with caps and floors to limit gains and losses. On the other hand, Whole Life insurance provides a guaranteed rate of return on the cash value, offering more stability but typically lower growth potential.

- Premium Flexibility: IUL policies offer premium payment flexibility, allowing policyholders to adjust their payments within certain limits based on their financial situation. Whole Life policies have fixed, consistent premiums that do not change over the policy's life.

- Risk: IUL carries more risk due to its exposure to market fluctuations, though it includes safeguards like floors to prevent negative returns. Whole Life insurance is less risky, with guaranteed cash value growth and death benefits, providing more predictable and stable financial planning.

- Cost: Whole Life insurance generally has higher premiums compared to IUL due to its guaranteed cash value growth and fixed benefits. IUL can have lower initial premiums but may vary over time depending on how the policy is managed.

- Death Benefit Options: IUL policies often allow for adjustable death benefits, meaning the policyholder can increase or decrease the death benefit amount over time, subject to underwriting and policy guidelines. Whole Life policies typically offer a fixed death benefit that does not change.

- Policy Loans and Withdrawals: Both IUL and Whole Life policies allow for loans and withdrawals against the cash value, but the terms and impact of the policy can differ. IUL policy loans might be influenced by the index performance, whereas Whole Life policy loans usually have more predictable terms.

- Dividend Payments: Whole Life policies, particularly those from mutual insurance companies, may pay dividends to policyholders, which can be used to increase the cash value, reduce premiums, or purchase additional insurance coverage. IUL policies do not pay dividends; instead, their growth is tied solely to the index performance.

- Complexity and Management: IUL policies are generally more complex and require more active management and understanding of market indices and caps/floors. Whole Life policies are more straightforward, with predictable growth and fixed premiums, requiring less management from the policyholder.

These differences affect each type of policy's suitability depending on your financial goals, risk tolerance, and the need for flexibility.

Ready for Clarity? Uncover the ideal life insurance solution for your financial future. Get a Free Life Insurance Quote

Pros & Cons of IUL Insurance

Advantages

- Potential for Higher Returns: Tied to market index performance, offering the potential for greater cash value growth than fixed-rate policies like Whole Life.

- Flexibility: Adjustable premiums and death benefits allow for customization to meet your changing financial needs.

- Access to Cash Value: Can access cash value through loans or withdrawals, providing financial flexibility.

- Downside Protection: Most policies have a guaranteed minimum interest rate to protect against significant losses in the market.1

- Tax-Deferred Growth: Cash value growth is on a tax-deferred basis, meaning you don't pay taxes on gains until withdrawn.

- No Impact on Social Security Benefits: Unlike some retirement accounts, IUL withdrawals don't affect Social Security benefits.

Disadvantages

- Market Volatility: Returns are tied to market performance, meaning the cash value can fluctuate and may not grow as expected.

- Capped Returns: Most policies cap the maximum market return you can earn, limiting potential gains in a strong market.

- Complexity: More complex than other types of life insurance, requiring careful consideration and professional guidance.

- Potential for Lower Returns: In a poor market, the returns may be lower than traditional fixed-rate policies.

- Higher Fees: IUL policies typically come with higher fees than other life insurance types, which can reduce your returns.

- Requires Active Management: You may need to monitor your policy closely and adjust premiums or death benefits to ensure it performs as expected.

Pros & Cons of Whole Life Insurance

Advantages of Whole Life

- Guaranteed Death Benefit: Provides a guaranteed life insurance benefit payout to your beneficiaries upon your death, regardless of when it occurs.

- Guaranteed Cash Value Growth: Cash value accumulates at a fixed rate, providing a predictable and stable return.

- Fixed Premiums: Premiums remain the same throughout the policy's life, offering ease of predictability and budgeting.

- Potential for Dividends: Participating policies may pay dividends, which can be used to reduce premiums, increase cash value, or purchase additional coverage.

- Tax-Deferred Growth: Cash value growth is on a tax-advantaged basis, meaning you don't pay taxes on gains until withdrawn.

- No Impact on Social Security Benefits: Unlike some retirement accounts, Whole Life withdrawals don't affect Social Security benefits.

- Policy Loan Option: You can borrow against your cash value, providing access to funds in an emergency.

Disadvantages

- Premium Costs: Premiums are generally higher than other types of life insurance, making it a higher-cost option.

- Lower Potential Returns: Cash value growth is often lower than other investment options, limiting potential wealth accumulation.

- Less Flexibility: Premiums and death benefits are fixed, offering less flexibility than IUL policies.

- Surrender Charges: If you cancel the policy early, you may incur surrender charges, which can significantly reduce your cash value.

- Complexity: While simpler than IUL, Whole Life can still be complex, and it's important to understand the terms and conditions before purchasing.

- Slow Cash Value Growth: The cash value can take several years to build up significantly.

- Limited Investment Options: Your cash value is invested in the insurance company's general account, limiting your investment choices.

Which Policy Is Right for You?

Choosing between IUL and Whole Life insurance requires careful consideration of your financial goals, risk tolerance, and individual needs. Here are some key questions to ask yourself:

1. What Are Your Financial Goals?

- Wealth Accumulation: If you want to maximize your cash value growth potential, IUL may be more appealing due to its higher return potential.

- Guaranteed Protection: Whole Life might be a better fit if you prioritize a guaranteed death benefit and stable cash value growth.

- Retirement Income: If you plan to use your life insurance policy as a source of retirement income, IUL's potential for higher returns could be beneficial.

2. What Is Your Risk Tolerance?

- Risk-Averse: Whole Life's guaranteed growth and fixed premiums might appeal more if you prefer predictability and stability.

- Risk-Tolerant: If you're comfortable with some market risk and willing to sacrifice stability for the chance of higher returns, IUL might be a better choice.

3. How Important Is Flexibility?

- Need for Flexibility: If you anticipate adjusting your premiums or death benefit in the future, IUL offers that flexibility.

- Prefer Predictability: Whole Life offers that stability if you value knowing exactly what your premiums and death benefit will be.

4. How Much Are You Willing to Pay?

- Cost-Conscious: Whole Life generally has higher initial premiums than IUL, making it a more expensive option upfront.

- Open to Higher Costs for Potential Growth: IUL's potential for higher returns may justify its potentially higher long-term costs.

5. How Involved Do You Want to Be?

- Hands-Off Approach: Whole Life requires little to no ongoing management, making it a simpler option.

- Active Management: IUL requires more active monitoring and potential adjustments to premiums or death benefits to ensure optimal performance.

Conclusion

Choosing between IUL and Whole Life insurance is an important decision that requires thorough consideration of your financial goals and risk tolerance. By understanding each policy's key differences, benefits, and drawbacks, you can make an informed selection that provides the best protection for your future.

Contact a qualified life insurance agent to explore your options and find the ideal policy for you. They can help in assessing your needs and suggest the most appropriate policy for your specific circumstances.

Talk to an expert. Get personalized guidance on IUL vs Whole Life Insurance. Get a Free Life Insurance Quote

Footnotes

- The client can lose money with the product, just not due to declines in the indexes. The downside protection only extends to market losses. Insurance costs and charges will reduce account value, possibly resulting in a lapse if premiums and returns are insufficient. Avoid being overly promissory by specifying the protection that is offered.

- Withdrawals may be subject to charges, withdrawals of taxable amounts are subject to ordinary income tax, and, if taken before age 59½, may be subject to a 10% IRS penalty.

- Interest is charged on loans; they may generate an income tax liability, reduce the Account Value and the Death Benefit, and may cause the policy to lapse.