Table of Contents

Private College Tuition Cost

College may become a six-figure investment for many families. Meanwhile, tuition and fees for public in-state and out-of-state institutions range from about $11,610 to over $30,780 annually.1

When you consider that the current U.S. median household income is around $70,000, that means many families will have to plan carefully and save aggressively to cover college costs.2 But there's another source of college funding that may be worth considering — loans.

Both federal and private loans are available to help pay for college, but you should be careful about how much you and your child take out to fund their education, and make sure you all understand the repayment terms. Here are some items to consider when making this choice.

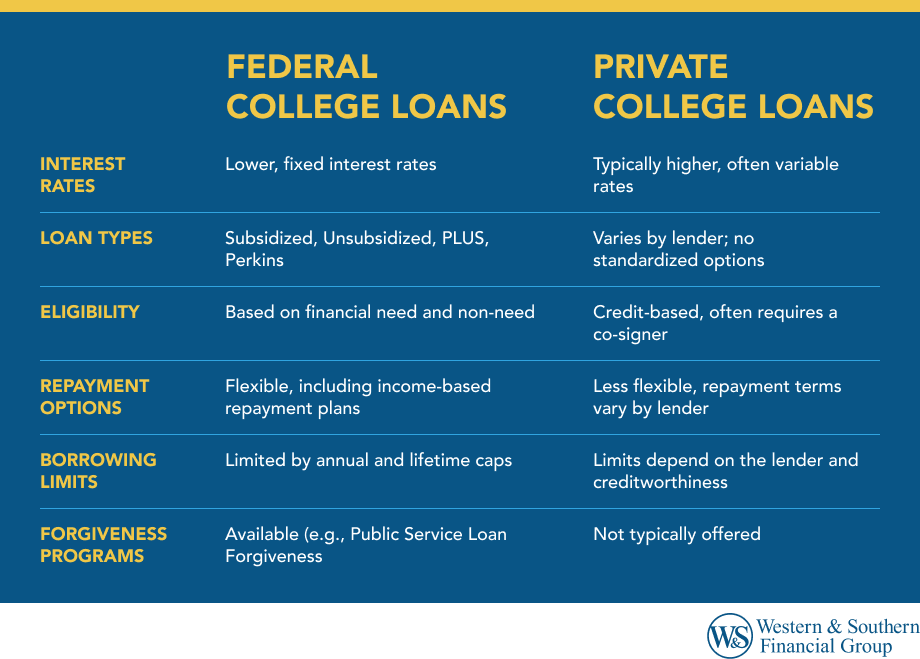

Federal College Loans

The federal government offers both need- and non-need-based loans. If you fill out the Free Application for Federal Student Aid (FAFSA), a school may award your child loans as part of their financial aid package if they plan to enroll in school either part- or full-time.3 Loans must be repaid after graduation, with interest rates and terms.

However, federal loans are typically less expensive to repay because they have fixed and lower interest rates than private loans (loans taken out from a bank). There are four types of federal college loans:

- Direct subsidized loans: Students with financial need can qualify for direct subsidized loans. A loan subsidy means the government pays the interest while your child is in school, during the grace period (the first six months after school) and during times your child defers or postpones loan payments (usually because of financial hardship or if your child decides to pursue an advanced degree).

- Direct unsubsidized loans: Direct unsubsidized loans are non-need-based loans available to undergraduate and graduate students. These loans begin to accrue compound interest even while your child is in school. Since the loans are unsubsidized, your child — not the federal government — is responsible for paying all the interest accrued throughout the life of the loan.

- Direct PLUS Loans: Graduate and professional students, along with parents of dependent undergraduates, can take out these loans to pay for college. The maximum amount you can take out is the difference between any financial aid your child receives and the total cost of attending the school. However, to qualify for these loans, you can't have a poor credit history.

- Perkins Loans: The Perkins Loan is a low-interest loan for students with high financial need. Unlike with the three other types of federal college loans, your child's school is the lender. The loan comes with a 5% interest rate. However, not every school participates in this federal loan program, so you'll need to check with each school's financial aid office to make sure they offer it.

Private College Loans

If your family isn't offered federal college loans, or what you're awarded isn't enough to cover your child's total college costs, you may need to consider private college loans.

Banks and other lending institutions offer these loans, and they typically have higher interest rates than federal college loans. Some lenders also offer loans with variable interest rates, meaning they change over the life of the loan and may gradually grow from a lower rate to a higher one. For example, some loans can have rates that increase from 3.99% to 12.99%.

Private loans are unsubsidized, meaning the borrower pays all interest. If you do co-sign, you may want to consider additional protections, like taking out a life insurance policy for your child.

With private loans, it's critical to understand the interest rate, terms and fees. Depending on your credit history, you may get a higher interest rate that increases the long-term cost of the loan. Also, some loans may charge an origination fee just to get the loan, or a fee if you pay off the loan early. Look for these details in the fine print as you shop around and compare loans. This will help your family make the best decision about how much to borrow and what lending institution to borrow from.

When Might You Take Out Loans?

Loans aren't free money — every dime your family borrows will have to be repaid, along with interest. It's important you begin planning for college tuition payments as soon as possible and carefully consider all the college funding options available.

Student Loan Debt

A 529 college savings plan allows you to make tax-deferred contributions and withdraw the principal and earnings to pay for qualified educational expenses, like tuition, room and board, a computer or books. You can withdraw the funds from the account at any time, but keep in mind that there are tax consequences if you do not use the money on qualified expenses. Government-backed savings bonds, which you can cash in tax-free to pay for college tuition and fees, are another option to put money away for your child's education.

The Bottom Line

The most important thing is to begin saving early, because you never know what kind of financial aid your child will qualify for, if they'll be awarded enough federal loans to cover all their college costs, or if the private loan options available are too expensive to repay over the long term. While loans are meant to help you pay for college — and the long-term benefits a college education can provide — it can still help to be mindful about how much you borrow.

Build a strong college savings foundation with the best loan options. Invest Today

Sources

- Highlights: Trends in College Pricing. https://research.collegeboard.org/trends/college-pricing/highlights.

- Income in the United States: 2023. https://www.census.gov/library/publications/2024/demo/p60-282.html.

- Complete the FAFSA® Form. https://studentaid.gov/h/apply-for-aid/fafsa.

- Student Loan Debt Statistics. https://educationdata.org/student-loan-debt-statistics.