Table of Contents

Table of Contents

You enjoy many options when shopping for permanent life insurance. It's possible to get coverage that lasts for your entire life (as long as you continue to pay the required premiums and other costs), ensuring a measure of protection for your beneficiaries upon your passing.

Two popular choices are universal life and whole life. Here's a closer look at one versus the other as well as insight into important questions, such as "can you cash out whole life insurance?" and "is one better for you than the other?"

What Is Whole Life Insurance?

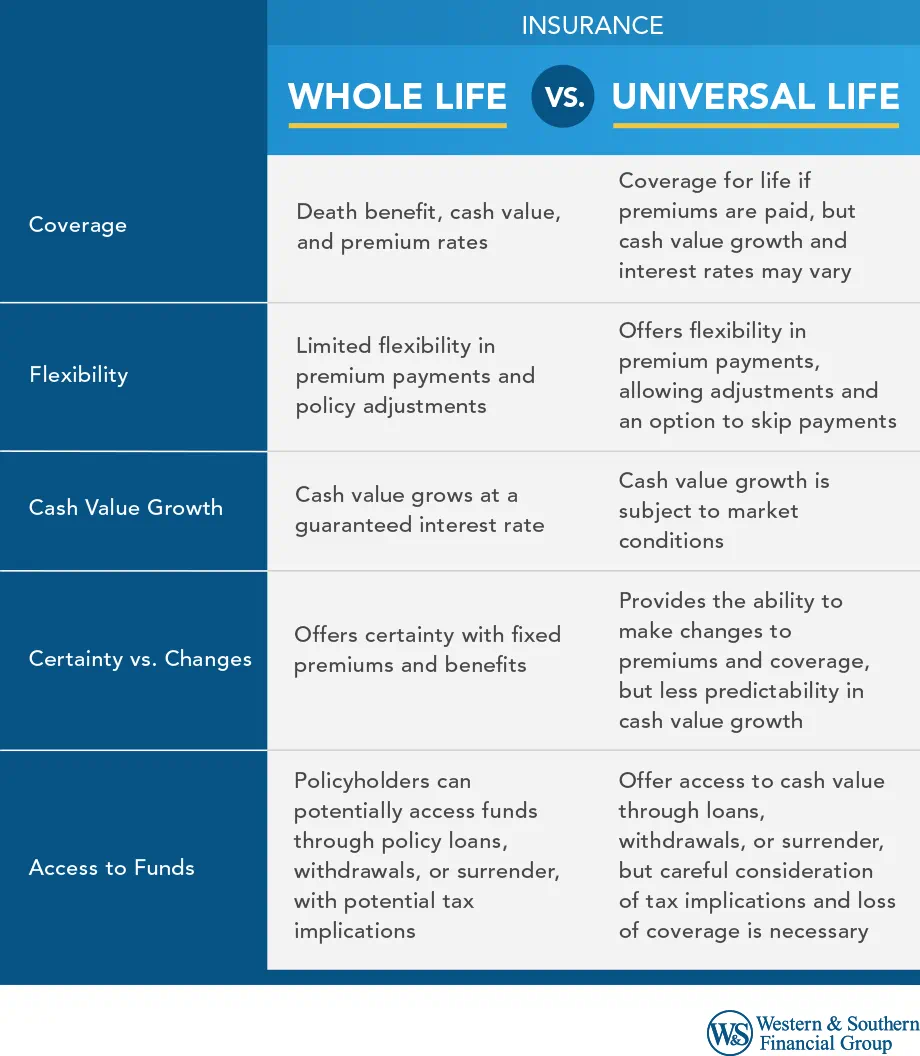

Whole life insurance is a permanent insurance contract with a guaranteed death benefit and cash value. As long as you pay the premiums required for coverage, the insurer will provide the benefits promised. Premiums are typically fixed for the life of the contract, which helps provide predictability as you manage your budget.

The cash value in a policy earns a fixed interest rate, which is guaranteed when the policy is issued so that you can anticipate your cash value in any given year.

What Is Universal Life Insurance?

Universal life insurance is a form of permanent coverage that offers some flexibility. As long as you pay the costs of insurance, your policy can remain in force for your entire life.

This type of insurance also provides policyholders with a cash value. The crediting rate on a universal life policy's cash value can change, so you often can't predict how much you'll have in cash value. Rates typically depend on economic conditions and interest rates, and the insurer can adjust rates over time.

What's the Difference Between Whole Life & Universal Life Insurance?

Both forms of coverage share a lot of similarities but also are distinguished by some key differences. For instance, whole life insurance is generally more predictable than universal life. Whole life policies have a guaranteed interest rate, guaranteed cash values and a guaranteed death benefit for any given year. All of those features are set when your policy is issued. They cannot be reduced unless you withdraw money from your contract. To get those guarantees, you must pay your scheduled premium as agreed.

Meanwhile, universal life can be more flexible than whole life insurance. For example, you might be able to reduce your premium payments — or occasionally skip premiums — without losing coverage. If your income is sporadic, it could make sense to pay into the policy when you have enough money and pause premium payments during periods with no income. However, if your policy runs out of cash value, the policy could lapse (with a potential loss of coverage and tax implications).

What's more, universal life does not guarantee your crediting rate in the same way as a whole life policy. Because of that, you might earn more or less than you expect, which can affect the amount you need to pay in premiums for better or worse.

Evaluate life insurance plans to match your long-term financial goals. Get a Life Insurance Quote

Is Whole Life or Universal Life Protection Better?

Your decision depends on your individual situation. The better choice of coverage effectively balances your needs, your comfort level with risk and other factors. If you prefer certainty, a whole life insurance policy might be a good fit. You can know in advance how much you'll pay in premiums and how much cash value you'll have at every stage. As long as you pay the premiums, you can be confident that the death benefit will be there when you need it.

If you prefer the ability to make changes, a universal life policy might make sense. Those contracts allow you to occasionally skip premium payments, which can be helpful when cash flow is tight. However, universal life policies lack the certainty of whole life coverage. So, you risk losing coverage or needing to make substantial payments into the policy if things don't go well.

Can you cash out whole life insurance? There are several ways to access funds from a whole life contract while you're still alive. For example, you can potentially borrow from the policy for a generally tax-free source of funds. However, it's critical to use policy loans with caution. If you withdraw too much, the policy could lapse. If that happens, you would both lose coverage and face possible tax consequences. Moreover, loans accrue interest, so borrowing funds might reduce the amount your beneficiaries receive after your death.

If you're not interested in a loan, you might be wondering if you can cash it out completely. Yes, it is possible to surrender a policy. However, doing so would end your coverage (and could also come with potential tax implications). You might also be able to take withdrawals from your policy's cash value, but if you withdraw more than you've contributed over the years, doing so could result in taxable income.1

The cash value in a universal life policy can potentially be tapped through loans, withdrawals and surrender as well.2 Keep in mind that the potential tax implications and loss of coverage described above also apply to universal life insurance. Again, it's critical to monitor your policy and analyze the situation before cashing out entirely.

The Bottom Line

Ultimately, the decision between universal life insurance versus whole life insurance depends on your needs. Evaluate the pros and cons of each option. Consider consulting with a financial professional to help determine what may be better for you and your family. Equipped with guidance and the information above, you may find yourself in a better position to make a well-informed choice.

Choose life insurance that grows with you and helps secure your legacy. Get a Life Insurance Quote

Footnotes

- Withdrawals may be subject to charges, withdrawals of taxable amounts are subject to ordinary income tax, and, if taken before age 59½, may be subject to a 10% IRS penalty.

- Interest is charged on loans, they may generate an income tax liability, reduce the Account Value and the Death Benefit, and may cause the policy to lapse.