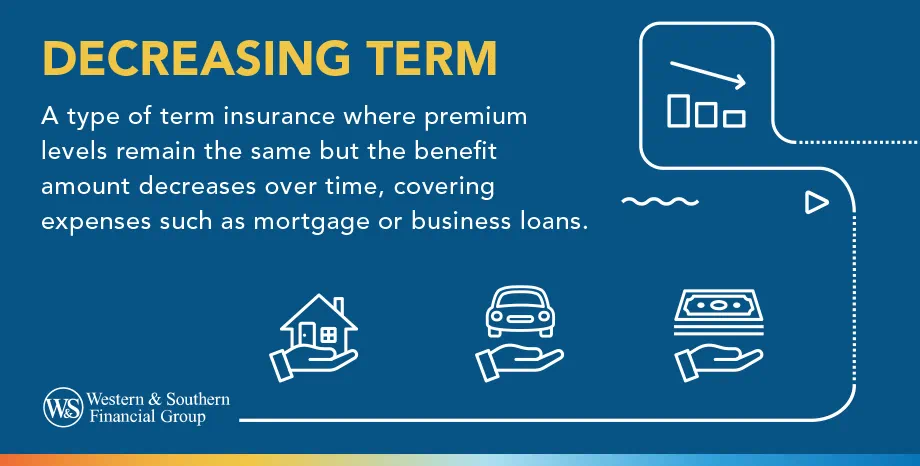

What Is Decreasing Term Insurance?

This type of coverage decreases over the life of the policy. It is often used to cover financial obligations that also decrease over time, such as a 30-year mortgage or business loans.

The key features and benefits of decreasing term insurance include its coverage decrease over the life of the policy, making it ideal for amortizing loans.

This type of insurance is also more affordable compared to level-premium term insurance, making it a cost-effective option for those looking to cover specific financial obligations.

How Does Decreasing Term Life Insurance Work?

Decreasing term life insurance is a policy that reduces the death benefit over time until it reaches zero.

- To set up a decreasing term life insurance policy, you will need to choose the policy length and starting death benefit. This could be based on factors such as your mortgage payments, student loans or other debts and financial obligations that decrease over time.

- You will also need to name beneficiaries who will receive the death benefit upon your passing.

- Once the policy is in place, you will pay regular premiums to keep the policy active.

- As time passes, the death benefit decreases, aligning with the reducing financial obligations of the policyholder. For example, if the policy is designed to cover a loan, as the balance decreases, so does the death benefit.

- Maintaining the policy involves keeping up with premium payments and reviewing the policy as financial obligations change.

- As the policy nears its end, the death benefit will approach zero, and at the end of the term, the policy will no longer provide coverage.

Overall, decreasing term life insurance provides a way to ensure financial protection for loved ones while matching the decreasing financial obligations over time.

Advantages of Decreasing Term Life Insurance

- Family Protection. One of the main benefits of decreasing term life insurance is its ability to protect mortgages or personal loans.

- Business Protection. Small businesses, and business partners, can benefit from decreasing term insurance, as it can help to fund continuing operations or cover any outstanding business debts.

- Affordability. Decreasing term life insurance is more affordable compared to other types of life insurance, such as whole life or universal life insurance. This makes it a cost-effective option for those with fluctuating financial needs.

Disadvantages of Decreasing Term Life Insurance

- Declining Coverage. As the policyholder pays the same price for less coverage over time, the value of the death benefit decreases as the remaining mortgage or loan diminishes. This means that, as the policyholder ages, the coverage may not be sufficient to meet the original intended needs.

- Limited Use. The death benefit is limited to only covering outstanding debts, leaving little to no room for the beneficiaries to use the funds for other purposes, such as daily living expenses or funeral expenses.

Cost of Decreasing Term Life Insurance

The cost of a decreasing term policy is influenced by several factors. The coverage amount and term length are key determinants, as a higher coverage amount and longer term typically result in higher premiums.

Poor health, risky behaviors, or an occupation with higher inherent risks can lead to increased premiums, as they can impact the likelihood of filing a claim.

Benefit from consistent premiums with decreasing coverage. Get a Life Insurance Quote

What Happens at the End of a Decreasing Term Life Policy?

At the end of a decreasing term life policy, the coverage terminates and the death benefit coverage ends. This means that the insurance company will no longer provide a payout in the event of the policyholder's death.

Throughout the duration of the policy, the amount insured decreases each year, typically aligning with a financial obligation. This means that as the policyholder pays off their debts, the coverage amount decreases accordingly.

At the end of a decreasing term life policy, the coverage and death benefit payout will have diminished in line with the decreasing coverage amount, and the policy will terminate.

Level Term vs. Decreasing Term Insurance: What's the Difference?

Level term insurance offers a consistent death benefit payout over the duration of the policy, while decreasing term insurance provides a death benefit that decreases over time.

Level term insurance policies typically last for a specific number of years, such as 10, 20, or 30 years, with the death benefit remaining unchanged throughout.

On the other hand, decreasing term policies are often used to cover a specific debt, such as a mortgage or loan, and the death benefit decreases in line with the decreasing debt amount.

Both types of insurance offer a guaranteed death benefit, but the payout structure, duration, and premium structure differ, making each type more suitable for specific financial needs.

What Are the Alternatives to Decreasing Term Coverage?

There are several alternatives to decreasing term coverage for life insurance:

- Level term life insurance provides a fixed sum assured over a specified term. The payout remains constant, making it suitable for those looking for consistent coverage.

- Increasing term life insurance, on the other hand, offers a sum assured that increases over time. This option can help to keep up with inflation and rising living costs.

- Permanent life insurance is a broader category that includes whole life and other types of policies that offer protection for the policyholder's entire life, along with the potential for cash value accumulation.

Each alternative has its own unique features and benefits, so it's important to carefully consider your needs and preferences before making a decision.

Is Decreasing Term Life Insurance Right for Me?

Decreasing term life insurance may be worth it for individuals with specific financial obligations that will decrease over time, such as a mortgage or business loan. It may not be worth the cost for individuals seeking long-term, consistent coverage or for those with fluctuating financial needs.

Conclusion

Decreasing term life insurance can be a suitable option for certain individuals with specific financial obligations, but may not be the best choice for everyone. It is important to carefully consider one's financial situation and future needs before deciding on the appropriate life insurance policy.

Determine if decreasing term life insurance matches your financial goals. Get a Life Insurance Quote