Table of Contents

Many millennials, born between 1981 and 1996, face financial challenges due to factors like student loan debt and entering the job market during the Great Recession. Despite this, millennials are actively prioritizing retirement planning. They are increasing their retirement savings, especially through Roth IRAs.

Proactive Approaches and Valuable Insights

While millennial retirement may be distinct from previous generations, there are valuable lessons that all future retirees can learn from their proactive approach. These include knowing the appropriate Roth IRA contributions, recognizing the significance of financial literacy, and consistently working towards financial independence goals.

Millennials have been committed to retirement savings — even with the pandemic's influence on the job market. According to research, the number of Roth IRA accounts held by millennials increased contributions by 17.7% in the beginning of 2024.1 The average 401(k) savings rate among this age group was 12.7, including employer contributions. Additionally, the average balance held by millennials was $62,000. This shows solid growth within the demographic but also room for development.

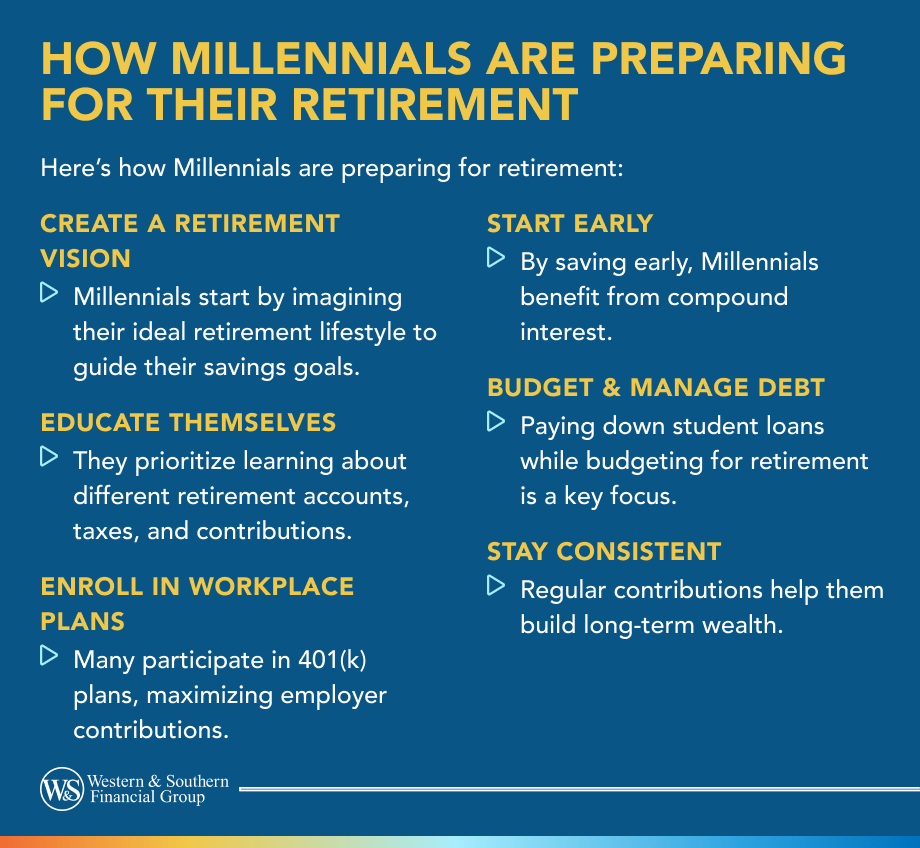

6 Millennial Retirement Planning Strategies

These trends provide key lessons for how workers of all generations can better prepare for the future. Here are six strategies to consider when planning your approach to retirement saving:

1. Create Your Vision for Retirement

Start by imagining the retirement lifestyle you want to have. Would you like to retire early, or do you think you'll shift to another career? Maybe you'll retire fully and move to a foreign country. Or you might see yourself spending retirement right where you are.

These considerations should play a role in how you save for retirement. Take the time now to envision what you want for your future and use it in developing your retirement plans.

2. Educate Yourself

Every future retiree should consider their options. You'll have an edge if you know a bit about the different types of retirement accounts, how they work with taxes and how much you can contribute. For example, employers typically offer 401(k) plans, but anyone with earned income can open an IRA. You can invest pre-tax dollars in a traditional IRA or put after-tax dollars in a Roth IRA. Each has different advantages and limitations.

It's also good to understand the basic difference between stocks and bonds. Knowing how to allocate between them within your portfolio can give you more control. Having a firm grasp of the investment options available to you can go a long way toward helping you reach your retirement goals.

3. Start Saving Early

Millennials are on the right track: Saving early can lead to building up a retirement account considerably quickly. Recall that millennials in late 2021 were sitting on an average $382,800 in their retirement accounts.

Average Retirement Savings

Though it isn't guaranteed that any market-based investment will increase in value, compound growth is a powerful tool that potentially can benefit your retirement savings over time. With that in mind, starting early usually means you can put in just a little bit of money every month to reach your retirement goals later. If you don't start saving until you're closer to retirement, you'll likely have to invest more every month to catch up to where you want to be.

Depending on your income and expenses, it may be more challenging to save a large amount every month as you near retirement. So take a note from millennials and start saving as early as possible to give your retirement savings more time to potentially grow.

4. Enroll in a Workplace Retirement Plan

Many millennials have IRAs but are also enrolled in their employers' retirement plans, often a 401(k). If this option is available to you, consider taking advantage of it.

Employers that offer retirement plans often match contributions up to a certain percent of your salary. Let's say your employer offers a 401(k) match up to 5%. If you make $50,000 a year and are putting at least 5% of your salary into your 401(k), your employer is tossing an extra $2,500 — essentially free money — into your retirement account for you.

Another benefit of participating in an employer-based plan is that it can reduce your taxable income. This could give you more money to invest in subsequent years. Using an employer's plan can also help you avoid account costs. Because employers often pre-select plan options and have HR field any questions, there usually aren't administration fees for you.

5. Budget & Tackle Debt

Millennials wouldn't have been able to increase their retirement contributions in recent years if they didn't have extra money to put toward investing. One likely explanation for where this extra money comes from is budgeting and paying down debt.

Average Millennials Debt

Paying down debt requires effective budgeting and accounting for where every dollar goes. Although getting rid of debt is hard, it shouldn't be a barrier to saving for retirement. If you have any extra money, whether it's $50 or $500, consider allocating some or all of it to retirement. The more you save now, the more time your investments can have to grow and help provide the financial stability you need to enjoy retirement. Of course, investments cannot guarantee growth or sustainment of principal value; they may lose value over time. Past performance is not an indication of future results.

6. Stay the Course

The retirement planning trend among millennials shows how important it is to stay the course and keep working toward your goals. Like generations before them, millennials have seen the market go up and down. Yet many of them have continued saving for retirement through both good and bad times.

The lesson here is that although there are no guarantees when investing, saving early (and often) and avoiding panic when market shifts occur can help promote effective retirement planning. Being consistent could make all the difference for your retirement savings, too.

Navigating Your Retirement Journey

Your retirement may be years or even decades away, but that doesn't mean you shouldn't start planning now.

Millennials have clearly gotten a jump on retirement planning and have focused on saving for retirement alongside tackling other financial priorities. They've contributed to their workplace retirement plans and opened IRAs to increase their savings, even considering how much to contribute to a Roth IRA so they can benefit from tax-free withdrawals in retirement.

Their example shows it's never too early to start saving and that it's important to stick to your plan as closely as possible — even when times get tough. By doing so, you can better prepare for your financial future and make your vision for retirement a reality. If you think you could use some help with retirement planning, consider contacting a financial professional who can take a customized look at your situation.

Having a structured retirement plan helps you achieve long-term financial stability. Start Your Free Plan

Sources

- Building Financial Futures. https://www.fidelityworkplace.com/s/page-resource?cId=fidelity_building_financial_futures_report.

- What Is the Average Retirement Savings in the U.S.? https://www.fool.com/research/average-retirement-savings/

- Experian Study: Average U.S. Consumer Debt and Statistics. https://www.experian.com/blogs/ask-experian/research/consumer-debt-study/.