Many people believe their assets will automatically go to the right person after they die, but that is not always the case. Selecting beneficiaries is a legal decision that affects your legacy.

Understanding the difference between primary and contingent beneficiaries can help prevent family disputes, probate delays, and unintended outcomes.

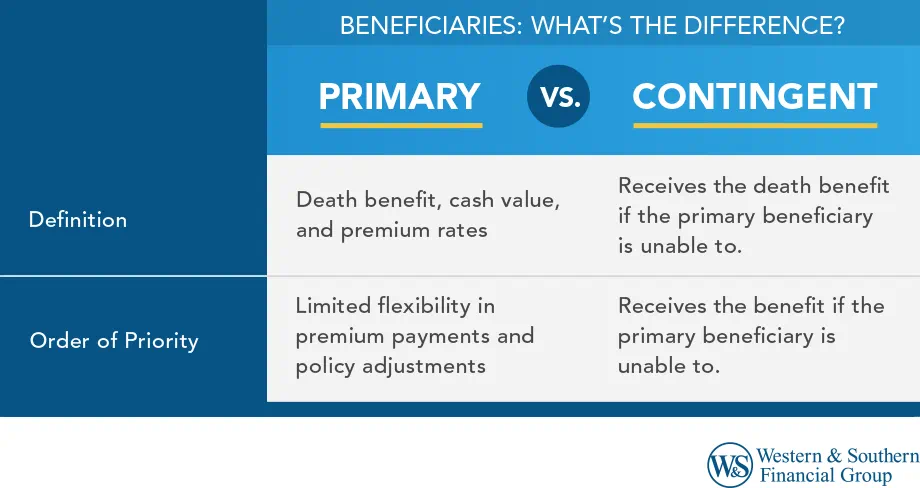

What Is a Beneficiary?

A beneficiary is a person or entity you choose to receive assets, such as life insurance payouts or retirement benefits, after your death. You can name multiple beneficiaries and decide how they will share your assets.

There are two main types of beneficiaries:

- Primary Beneficiaries: The first in line to receive assets such as death benefit proceeds.

- Contingent Beneficiaries: A backup who receives assets if the primary beneficiary has died or cannot accept them.

These designations are common (but not limited) to in:

- Life insurance policies and annuities

- Retirement accounts such as IRAs and 401(k)s

- Living trusts

- Brokerage and bank accounts

- Legal documents related to estate planning

Naming primary and contingent beneficiaries clarifies asset distribution, minimizing legal disputes or delays. This may allow your loved ones to focus on healing instead of legal or financial complexities. When it comes to life insurance or retirement accounts, choosing your beneficiaries wisely is crucial for a smooth estate planning process.

Who or What Can Be a Life Insurance Beneficiary?

Life insurance policyholders have flexibility when choosing beneficiaries. Here are some common examples:

- Spouses: Married couples often name each other as primary beneficiaries.

- Children: Children are often listed as contingent beneficiaries, but they can also be primary beneficiaries.

- Other Relatives: This may include siblings, parents, or extended family members.

- Nonrelatives: You are not required to name a family member. You can choose anyone.

- Trusts: A trust can manage the death benefit for minor children or others who need guidance handling funds.

- Organizations: Charities, nonprofits, or businesses can be named as beneficiaries.

- Employers: In some cases, an employer may be the beneficiary of a policy designed to help protect the business.

You have many options when naming beneficiaries. It may help to speak with a professional who understands insurance products before choosing a policy.

Why Do Both Designations Matter?

Many people only name a primary beneficiary and leave the contingent section blank. This can lead to problems such as:

- Death Benefit Payout Delays: Without a backup, if no valid beneficiary is designated, proceeds may need to go through probate, depending on state laws.

- Legal Complications: Courts may need to decide who receives the assets.

- Estate Taxes: Assets without direct beneficiaries may be included in your taxable estate.

- Emotional Stress: Loved ones are left to untangle complex legal issues during an already difficult time.

Consider adding contingent beneficiaries to your estate’s insurance policy.

How to Choose the Right Beneficiaries

Choosing who will inherit your assets is both an important and thoughtful decision. Here are a few friendly tips to help you make the right choices:

- Relationship: Start with close family members such as a spouse, children, or siblings. You may also consider trusted friends or charities.

- Age: Minors cannot directly receive assets. You may need a trust or legal guardian to manage funds until they reach adulthood.

- Health: If a primary beneficiary has serious health concerns, naming a contingent beneficiary becomes even more important.

- Financial Responsibility: Consider whether your beneficiary can manage the assets. A trust may help if you have concerns.

- Life Events: Review your choices after major events such as marriage, divorce, birth, or death.

Also keep the following in mind:

- Check Your Information: Make sure names are spelled correctly. Small errors can cause delays or confusion.

- Be Clear About Distribution: List percentages that add up to 100%.

- Include Identifying Details: Add information such as Social Security numbers to avoid confusion.

Reviewing and updating your beneficiary designations regularly can help keep them aligned with your wishes.

What Happens If No Beneficiary Is Named?

Choosing a beneficiary when you apply for life insurance might appear straightforward, but there are occasions when beneficiaries aren't designated. If no primary or contingent beneficiary is named, or if both have passed away:

- The asset/death benefit proceeds will become part of your estate and will have to go through the probate process.

- A judge will decide how to distribute the asset/death benefit proceeds, generally following the state's intestacy laws.

- The probate process might slow things down a bit, with distributions taking a few extra months.

- Your loved ones may encounter some estate taxes or legal hiccups. Depending on your estate size and structure, there may be estate tax implications. Consult your tax advisor for personalized guidance.

To prevent these issues, it is important to complete your beneficiary forms now, even if you are young and healthy. Clearly designating primary and contingent beneficiaries ensures your assets are shared as you intended, sparing your loved ones the stress and delays of probate.

Tips for Naming Life Insurance Beneficiaries

When naming life insurance beneficiaries, here are important points to keep in mind:

- Read the form carefully. It's important to read your beneficiary form carefully and scrutinize its language before filling in names and percentages, as not all forms are designed the same.

- Always name a beneficiary. Dying without a beneficiary can subject the policy to the probate process, leading to extra costs, delays, and possibly unfavorable taxation.

- Name both primary and contingent beneficiaries. Naming a contingent beneficiary helps ensures your assets/death benefit proceeds go your desired parties, if the primary beneficiary is unable to receive it.

- Consider tax benefits and consequences. Beneficiaries typically don't pay taxes on a life insurance death benefit, but naming an estate instead of an individual could lead to estate tax liabilities for the inheritors.

- Coordinate beneficiaries with your will or trust. When you're naming life insurance beneficiaries, consider tax effects and sync with your estate plan to ensure asset distribution and avoid probate issues.

- Avoid naming your estate as your beneficiary. It's generally best to have assets pass to beneficiaries directly to avoid probate, which could distribute benefits differently than you planned.

- Trusts are generally not ideal as life insurance beneficiaries. Help ensure your life insurance policy coordinates with your estate plan to avoid probate, and consult an expert for tax implications and the appropriateness of naming trusts.

Final Thoughts: Your Legacy in the Details

Choosing between a primary vs. contingent beneficiary isn’t just a formality. It’s a thoughtful decision that can shape how your loved ones remember you, and how quickly they get the support they need after you’re gone.