Table of Contents

Understanding Key Financial Concerns

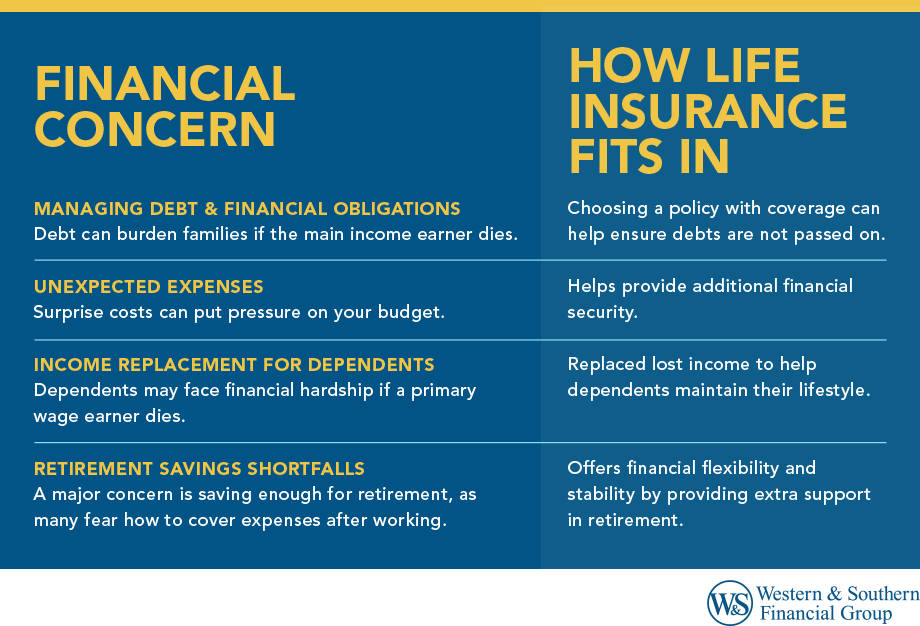

Financial management involves planning for both expected and unexpected expenses. Achieving stability through retirement savings, debt, and major life events requires careful consideration. Here are common financial concerns:

Managing Debt & Financial Obligations

Many people have significant financial obligations, including:

- Mortgage payments

- Student loans

- Credit card debt

- Auto loans

- Personal loans

If the primary income earner dies, these debts can financially burden surviving family members.

When selecting life insurance coverage, choosing an amount that covers major life events and future financial needs is important.

Emergency Savings & Unexpected Expenses

Life is unpredictable, and financial setbacks can happen at any time. Everyday unexpected expenses include:

- Medical emergencies

- Job loss

- Home or car repairs

- Unexpected family needs

While an emergency fund is important, life insurance is designed first and foremost to provide a death benefit that can help protect your loved ones financially if something happens to you.

Income Replacement for Dependents

If a primary wage earner passes away, their dependents may face financial hardship. Life insurance helps mitigate this risk by replacing lost income for a period of time, allowing families to maintain their standard of living.

When choosing the right type of policy, factors such as life expectancy, family history, and health issues should be considered. A term life policy is often affordable for young families, while permanent policies provide lifetime protection with additional financial benefits.

Example: Michael, a 35-year-old marketing executive earning $120,000 annually with two young children and a mortgage, purchased a $2 million 30-year term policy for $125 monthly. When he died unexpectedly at 42, the death benefit allowed his wife to pay off their mortgage, establish college funds for their children, and invest the remainder to generate replacement income, preventing financial catastrophe during an already challenging time. For illustrative purposes only and that actual results will vary.

Retirement Savings Shortfalls

A major financial concern is saving enough for retirement. Many worry about covering expenses after work ends. 401(k)s and IRAs are important; some may seek additional benefits to enhance their savings.

Choosing the right type of policy can provide financial flexibility and long-term stability for those concerned about running out of money in retirement.

How Life Insurance Can Address These Financial Concerns

Life insurance can help protect your family and finances by providing coverage that meets specific needs. Here are ways life insurance can help:

How Life Insurance Can Help with Retirement Savings

Life insurance can supplement retirement planning by offering financial benefits beyond traditional savings accounts. Here’s how different policies can provide additional support:

- Builds Cash Value - A variable life insurance policy accumulates cash value over a period of time, which policyholders may access in retirement. Cash value may take years to accumulate.

- Provides Lifetime Coverage - Unlike a term life policy, which lasts for a set term, a permanent life insurance policy stays in place as long as premiums are paid.

- Offers Additional Benefits - Some policies allow riders access to the death benefit for chronic or terminal illnesses.

Selecting the right type of policy can add flexibility and financial security to retirement planning.

Term Life Insurance for Income Protection

A term life insurance policy covers a set period, often 10, 20, or 30 years. It's popular for its affordability and simple benefits. With lower rates than permanent insurance, it's a practical choice for those needing coverage during their peak earning years.

Here’s how a term life policy can help:

- Covers Outstanding Debts - The death benefit can be used to pay off mortgages, loans, and other financial obligations.

- Reduces Financial Stress - Helps surviving family members avoid financial hardship.

- Provides Temporary Coverage - A term life policy lasts for a set period of time, often aligning with major financial responsibilities (e.g., mortgage term).

- More Affordable Premiums - Compared to permanent policies, life insurance rates for term policies are typically lower.

Permanent Life Insurance for Long-Term Financial Stability

Permanent life insurance policies, such as whole life and universal life, offer benefits beyond just a death benefit. These policies provide:

- Lifelong Coverage - Unlike term life insurance, these policies last for your entire life as long as premiums are paid.

- Cash Value Growth – Over time, part of your premium builds cash value that can be accessed if needed.

- Supplemental Retirement Funds – Some policyholders use the cash value to supplement retirement income.

- Flexibility for Future Expenses – The accumulated cash can help cover unexpected costs or financial goals.

If you’re looking for a type of coverage that offers protection and savings potential, permanent life insurance could be an option.

Using Life Insurance as Part of an Estate Plan

Life insurance can play a key role in estate planning by helping cover costs and helping ensure your loved ones receive their inheritance without financial strain.

Here’s how a life insurance policy can help:

- Covers Estate Taxes - Helps heirs pay estate taxes without selling assets.

- Pays Final Expenses - Covers funeral costs, medical bills, and outstanding debts.

- Provides a Tax-Free Payout - The death benefit is generally tax-free for beneficiaries.

- Helps Protect Family Assets - Helps ensure loved ones don’t have to liquidate property or investments to cover expenses.

By choosing the right type of policy, you can ease the financial burden on your family and help secure your financial future.

Comparing Life Insurance Policies for Different Financial Needs

| Type of Life Insurance | Coverage Duration | Cash Value? | Premiums | Best For |

| Term Life Insurance | Fixed period of time (e.g., 10, 20, 30 years) | No | Lower | Individuals seeking affordable, temporary coverage |

| Whole Life Insurance | Lifetime | Yes | Higher | Those looking for permanent coverage with a savings component |

| Universal Life Insurance | Lifetime | Yes* | Adjustable | Individuals who want flexibility in premiums and death benefits |

| Variable Life Insurance | Lifetime | Yes (invested in market options) | Higher, fluctuates with investments | People comfortable with investment risks who want cash value growth potential |

* The policy must maintain sufficient cash value to cover charges, and that returns are not guaranteed.

Choosing the Right Life Insurance Policy

Choosing the right life insurance policy involves knowing your financial needs, budget, and goals. The ideal offers sufficient protection while matching your financial situation. Here are important factors to consider.

Factors to Consider When Selecting Coverage

Several factors influence the cost of life insurance, including:

- Health & Medical Background - Family history and health issues can impact eligibility and life insurance premiums.

- Age & Life Expectancy - Younger individuals generally get lower life insurance rates since they are considered lower risk.

- Type of Policy - Life insurance costs vary between term life insurance, whole life, universal life, and variable life insurance policies.

- Budget & Affordability - Consider what you can comfortably pay in life insurance premiums over a period of time.

Many insurers require a medical exam to assess your health status, which can affect your premium rates.

How to Calculate the Right Coverage Amount

Determining the right life insurance coverage helps ensure your family is financially help secure in case of unexpected events. Consider the following:

- Major Life Events - Marriage, home purchase, having children, and retirement planning all impact coverage needs.

- Outstanding Debts – The policy should cover mortgage, student loans, and credit card balances.

- Income Replacement - A common rule is to get a policy worth 10–15 times your annual income to cover long-term expenses.

- Future Expenses - Consider college tuition for children, spouse’s retirement, and medical costs.

By evaluating these factors, you can choose the type of coverage that best fits your financial goals.

Final Thoughts

Financial concerns impact many, but life insurance can alleviate these issues. Choosing the right policy, whether income replacement or savings, is important for financial stability. Knowing the differences in the types of policies and their costs could help lead to better financial protection.

Ease financial concerns with the right life insurance. Get a Free Life Insurance Quote