Preparing for retirement typically involves decades of saving for the future. If you're like most people, you focus on adding money to dedicated accounts and investing for long-term growth during that time.

But when you stop working, things change. Instead of building savings, you shift to retirement decumulation strategies. Decumulation is the process of spending down the assets you have built over your lifetime. As you manage your asset allocation in retirement, you need to cover basic needs like food and health care. You may also want to spend on things you enjoy, such as entertainment and travel.

Advantages of the Decumulation Stage

Retirement decumulation strategies can help you use the savings from your working years. There are several reasons to approach this stage with care:

- Design the life and schedule you want without relying on a paycheck

- Spend with more confidence when you have income sources that can last for life

- Use steady income sources instead of relying only on market performance

- Review the value of your home equity, which may be one of your largest assets

It is important to make sure your money lasts for the rest of your life. You may need to use new tools and adjust your asset allocation in retirement.

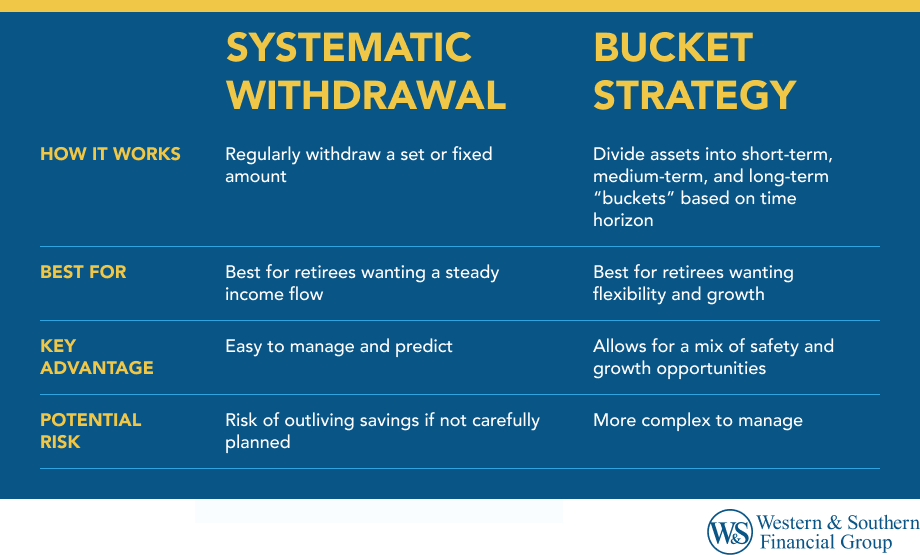

2 Decumulation Strategies to Consider

The shift to the decumulation stage can feel uncertain. With a clear strategy, you can feel more comfortable using the savings you have built. Different tools and approaches can support you during retirement. Here are two strategies to consider.

1. Securing Lifetime Income Sources

Lifetime income can play an important role in retirement. If you know income will continue for as long as you live, you may feel more confident about spending. Common sources include:

- Social Security: Available to most workers and includes inflation adjustments. Your benefit depends on your work history and the age you begin taking it.

- Pensions: Also called defined benefit plans. These are less common today, so many people rely more on personal savings.

- Annuities: These allow you to turn savings into a stream of payments with help from an insurance company. Some options can include payments for a spouse and features like death benefit.

The main advantage of lifetime income is that payments continue for as long as you live. You may want to align these income sources with your basic expenses.

2. Drawing Down Savings

You can also take money from retirement accounts such as individual retirement accounts (IRAs) and 401(k) plans. These funds may support your regular income or cover larger expenses like travel or home updates.

Spending from savings can be complex because of several unknowns. Market performance can change over time, and withdrawing money during a downturn may reduce your savings faster. You also do not know how long you will live or what unexpected costs may come up.

You will need to decide how much to withdraw each year. To estimate this amount, review your comfort with risk, use a retirement calculator , and talk with a financial professional. If you want more predictable income, you may consider adding a lifetime annuity to your asset allocation in retirement. This can help your income last as long as you do.

Bottom Line

Moving from saving to spending requires a shift in how you manage risk. One way to support long-term success is to have steady income that covers your basic needs. From there, you can decide how much of your savings to keep invested in the market.

If you want guidance, consider speaking with a financial professional who can review your situation and help you build a strategy.